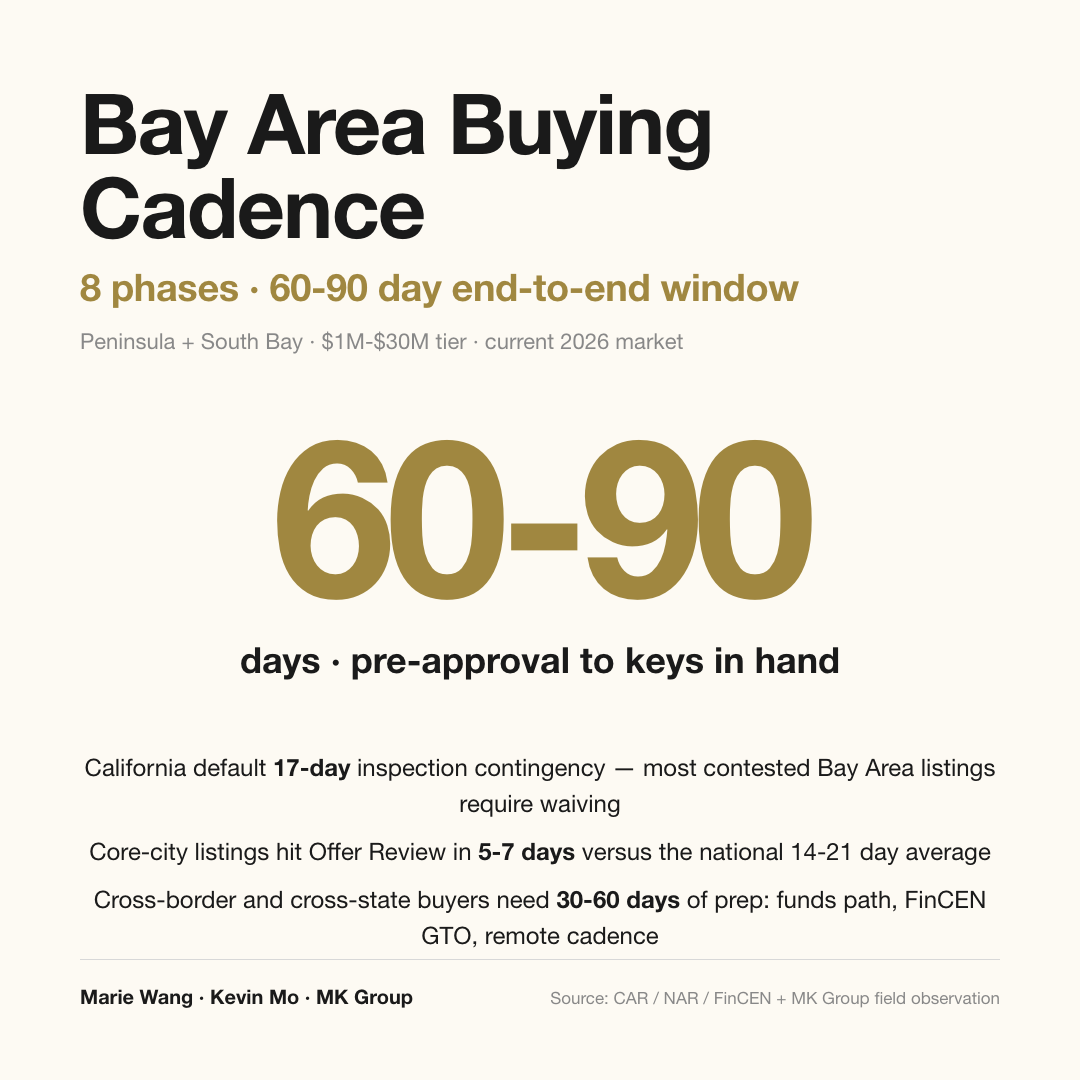

The Bay Area Home-Buying Process: 8 Phases, Typically 60-90 Days

The complete Bay Area home-buying process runs through 8 phases: pre-approval (financial prep), agent selection plus Buyer Representation Agreement, search and showings, disclosure due diligence, offer strategy, escrow open, final underwrite plus appraisal plus walk-through, and closing. End to end, the typical window is 60-90 days; cross-border and cross-state buyers usually need an additional 30-60 days of front-loaded preparation. This article is not a first-time buyer's weekly calendar — it is a phase-driven reference that breaks down what happens, what it costs, how long it takes, and what most commonly goes wrong at each stage. It applies to five buyer types: first-time, move-up, cross-border, cross-state, and investment.

Who This Guide Is For

This article serves five Bay Area buyer profiles. First-time buyers arriving with zero process experience who need a full-picture map of every phase — if your primary question is "what do I do each week," pair this with our companion piece, the first-time-buyer 8-week roadmap. Move-up families buying for the second time but discovering that the market and contract terms have changed materially (the NAR settlement, inspection-contingency culture shifts) and need an update on what's new. Cross-border buyers arriving from mainland China, Hong Kong, Singapore, or Taiwan who need 30-60 days of front-loaded prep on compliant funds paths and remote showing cadence. Cross-state relocators from Seattle, New York, Austin, or Boston whose employer permits remote or transfer, where the move is driven primarily by school decisions. Investment buyers not occupying the home, where ownership structure (LLC vs. trust vs. personal name), rentability, and long-term appreciation drive the decision.

Phase 1 — Pre-Approval and Financial Prep (W -8 to W -4)

Phase 1 starts 4-8 weeks before your first showing. The goal is to convert "how much house can I afford" from vague to precise and to come out with a pre-approval letter that holds up in a Bay Area bidding environment. Pre-qualification versus pre-approval is the first distinction to lock down. Pre-qualification is a soft, self-reported assessment that produces a five-minute online estimate — most Bay Area listing agents will not accept an offer attached to one. Pre-approval is the hard commitment a loan officer issues after actually reviewing your W-2s, tax returns, bank statements, and credit report; lenders generally turn one around within 24 hours, and that is the document that gets you into the bidding pool.

Three lender channels to compare: major banks (Wells Fargo, Chase, BofA), mortgage brokers (RPM, loanDepot), and portfolio lenders (local banks underwriting jumbo loans against their own balance sheet). Evaluate on four axes — interest rate (fixed vs. ARM), closing cost ($8K-$20K in points, origination, and appraisal), responsiveness (24-hour pre-approval turnaround is the Bay Area baseline), and loan officer experience with high-priced jumbo files. DTI ceiling: a monthly payment (including property tax, insurance, and HOA) at or below 33% of after-tax household income is conservative; 35% is aggressive. For a dual-engineer Bay Area household earning $450K pre-tax, after-tax monthly income lands around $26K, conservative monthly payment ceiling about $8,600 — translating to roughly $1.7M-$1.8M in purchasing power at 20% down and 6.5% rate.

Cross-border source-of-funds compliance is not a "I have the money" conversation. Title companies and escrow trigger FinCEN AML review on large international wires and require a complete source-of-funds declaration. The Corporate Transparency Act BOI filing requirement kicks in at the $300K+ LLC threshold. Run a small test wire ($10K range) 3-4 weeks before you start touring to validate channel timing and bank review behavior. All-cash buyers don't skip this phase either. Bay Area $5M+ luxury runs roughly 40-80% all-cash, mainstream $1M-$3M roughly 20-40% (MK Group industry-participant estimates, not MLS-sourced hard data). All-cash doesn't need a pre-approval, but it needs an equivalent proof of funds: statement screenshots, evidence the funds are deployable, and a pre-validated international wire path. Listing agents increasingly require POF attached to the offer itself.

Phase 2 — Agent Selection and Buyer Representation Agreement (W -4 to W -2)

The August 2024 NAR settlement requires California buyers to sign a Buyer Representation Agreement (BRA) before the first showing. This is the biggest recent process change — many families who bought before 2023 assume they can tour first and decide later, but without a signed BRA an agent cannot show MLS listings.

Three BRA dimensions to negotiate upfront. Duration: 30 days, 90 days, six months, and one year are all common — first-time engagements should run 30-90 days with renewal once the working relationship is established. Scope: which cities and which price ranges the agreement covers. If you're touring simultaneously across Palo Alto and Cupertino, scope must include both. Compensation: after August 2024, the buyer agent's commission is negotiated by the buyer directly, typically 2-3% of purchase price; whether the seller agrees to cover the buyer agent's commission is now case-by-case and one of the non-price levers at offer time.

When screening agents, look at local transaction volume over the last 24 months (5+ closings minimum), street-level familiarity with your target school zones (not city-level), cross-border or cross-state experience if it applies, bilingual capability for contract and negotiation work, and whether the team has dedicated buyer-side specialists. MK Group regularly meets buyers who didn't realize the BRA requirement existed until they tried to schedule their first showing. Doing a 30-minute intro call before signing — to confirm chemistry, working style, and BRA terms — prevents the "locked in" feeling that comes from signing under time pressure.

Phase 3 — Search and Showing Cadence (W -2 to Day 0)

Phase 3 typically runs 2-6 weeks from a signed BRA to a submitted offer. Bay Area showing cadence is the most local-specific stretch of the entire process.

Three listing sources to understand. MLS — the Multiple Listing Service, publicly listed inventory feeding Redfin, Zillow, Realtor.com. Transparent, most competitive, most complete information. Off-market — privately marketed properties not on MLS. Peninsula $5M+ off-market runs roughly 15-30% of inventory (MK Group industry-participant estimate, not MLS-sourced hard data), with the highest concentration in Atherton, Hillsborough, and Old Palo Alto. Accessed through agent networks. Pre-market (coming soon) — the 7-14 day preview window before listing date, where some buyer agents see listing previews.

The Bay Area cadence rule: in core cities (Palo Alto, Los Altos, Cupertino, Menlo Park) mainstream listings hit offer review within 5-7 days of going live — versus 14-21 days in most other states. This means a buyer has to decide to bid within 3-5 days of seeing a property. Waiting for "the next one might be better" in the core peninsula means at least 2-3 more weeks of search time. Cap showings at 15-20 homes; past 25, decision fatigue erodes judgment. Online pre-screening on Redfin, Zillow, and Google Maps Street View typically cuts 40-50% of candidates so only homes worth visiting in person make the calendar. Log three strongest pros and three biggest concerns immediately after each showing — details start blurring by the 10th home.

Cross-border buyers need a custom cadence. MK Group's Marie Wang has hosted families flying in from Asia who land in the morning and want to tour the same day; in one Shenzhen entrepreneur case, the brief was "show me $7M-$9M Peninsula luxury in half a day." Marie pulled four representative properties from MLS and off-market inventory covering Menlo Park, Palo Alto, Los Altos Hills, and Los Altos, sequenced them deliberately cheapest to most expensive, and built the family a mental map of the Silicon Valley luxury market in one afternoon. The goal of a cross-border first tour is not to bid that day — it is to build a judgment framework that the buyer can then operate from over the following months.

Phase 4 — Disclosure Due Diligence (Parallel to Phase 3)

Phase 4 runs in parallel with Phase 3 showings, but most buyers don't realize it — pushing disclosure review to post-offer inspection is the single largest knowledge gap in the Bay Area process. California disclosures are statutory mandatory reading, and listings should make them available the day the property goes live.

The mandatory disclosure pack: TDS (Transfer Disclosure Statement) — California-mandated seller disclosure of known physical defects. SPQ (Seller Property Questionnaire) — a more detailed seller questionnaire covering noise, neighbor disputes, and historical repair records. NHD (Natural Hazard Disclosure) — earthquake, fire, flood, and Mello-Roos special tax zones. Atherton, Portola Valley, and Woodside parcels within 5 miles of a fault line all require NHD. Pre-listing inspection report — Bay Area standard practice, paid for by the seller. Note that what the buyer sees may be a curated version; the buyer's agent needs to verify completeness of the reroof, HVAC, and major system sections. HOA documents, CC&Rs, and Estoppel Certificate — applicable to HOA properties only. CC&Rs define HOA restrictions; the Estoppel reveals current HOA financial health.

Street-level school district lookup is the single most overlooked buyer due-diligence step. MK Group worked an Atherton Oaks school-boundary diligence case where the buyer fell in love with a 94027 property in the town's center; on inspection, Atherton as a town spans three different elementary districts (Las Lomitas, Menlo Park City, Redwood City) and elementary assignment is determined street by street. The buyer's first-choice home sat on the wrong side of the boundary; comparable homes one block over on the correct side were trading roughly $1.5M higher. Zip code does not equal school district, and city level is not granular enough — verification has to be at the street-level attendance area. AOR tools or the city's official GIS can confirm.

Phase 5 — Offer Strategy and Submission (Day 0-3)

From deciding to bid to offer accepted or counter-issued usually takes 1-3 days. This is the information-density peak of the entire process.

Multiple-offer culture: in core Bay Area submarkets, 60-90% of strong listings see competing offers. Non-price levers often decide the winner. Contingency decisions — inspection, loan, and appraisal contingencies are each binary: keep or waive. Waiving raises offer competitiveness but transfers 100% of the underlying risk to the buyer. Close date — match seller preference; if the seller's downstream purchase is locked, a 21-day close beats a 30-day close. Rent-back — letting the seller stay 30-60 days post-close at no charge is one of the strongest non-price levers. Earnest money — California standard is 1-3% of purchase price, but a buyer can post more (say 5%) as a signal. Personal letter ("love letter") — write to the seller. Important caveat: since 2021, several California cities have raised fair-housing concerns about personal letters and some listing agents now refuse them outright. Confirm legal status with your agent before drafting.

Pricing ladder methodology: pull comparable sales from the last 90 days in the same zip code, adjust for size, lot, condition, and school attendance area, estimate the over-list ratio (core Bay Area submarkets are running 8-25% over list on strong 2026 listings, with wide dispersion), and decide what premium you're willing to pay — this depends on long-term holding intent, cash reserves, and read of competitor psychology. Counter-offer / highest-and-best flow: after collecting offers, the listing agent may accept directly or issue counters or call for best-and-final. Buyers have to respond within hours. Set your maximum ceiling with your agent before offer day, so you don't make a six-figure decision in real time at 9 PM.

Phase 6 — Escrow Open and Earnest Money (Day 3-7)

With offer accepted, the deal enters escrow. Open escrow: a third-party neutral (a title company or independent escrow company) holds funds and documents. In California most escrows are handled by the title company directly. Earnest money deposit: California typical is 1-3% of purchase price, mainstream is 3%, wired to escrow within roughly three business days. Earnest credits to the down payment at closing; if the buyer breaches unilaterally, the seller can claim it.

17-day inspection contingency window: California's default is 17 days — but on contested Bay Area listings, sellers typically require the buyer to waive at offer. This is the hardest single trade-off Bay Area buyers face. Waiving makes the offer more competitive but eliminates the structural-defect escape hatch. A common middle path: the buyer pays $400-$800 for a pre-inspection before submitting the offer, learns the risk profile, and then chooses to waive with eyes open.

Wire fraud warning: during escrow, both the buyer's inbox and the escrow officer's inbox are high-frequency targets. A common attack: hackers impersonate the escrow officer in email and provide "updated" wire instructions that route to the fraud account. Rule: any "account change" email must be verified by phone, calling escrow's main published number — never call the number in the email body. A hacked down-payment wire ($500K-$2M+) is functionally unrecoverable.

Phase 7 — Final Underwrite, Appraisal, and Walk-Through (Day 14-25)

This is where financed buyers most often hit surprises. All-cash buyers skip underwrite and appraisal and go straight to title and walk-through. Loan final underwriting: the pre-approval reflected your finances at that moment; final underwriting re-checks all documents — W-2s, tax returns, bank statements, credit report. Critical buyer behavior during this window: do not make major purchases, do not apply for new credit, do not change jobs, do not move down-payment funds. Any of these can collapse underwriting and the deal.

Appraisal report: the lender's appraiser values the property. If appraisal lands below contract price (which periodically happens in bidding markets), buyers have three options: negotiate the price down to appraisal value, cover the gap in cash (viable for cash-heavy buyers), or — if appraisal contingency was preserved — walk away and recover earnest money. Most strong Bay Area listings require the buyer to waive appraisal contingency, which means buyers must pre-plan "if appraisal comes in $200K low, can I cover that" — and that's exactly why cash reserve modeling belongs in Phase 1.

Title insurance and clean title search: the title company confirms the chain of title is clean (no unresolved liens, boundary disputes, unpaid taxes). Title insurance protects the buyer against future title defects. Final walk-through: 24-48 hours before closing, the buyer enters the property one last time to confirm the seller has vacated, agreed-upon fixtures remain, inspection-negotiated repairs were completed, and the property matches offer-time condition. If a major issue surfaces, the buyer can pause closing and request escrow credit or remediation.

Phase 8 — Closing and Recording (Day 25-30)

The final phase runs 3-5 days from signing closing documents to receiving keys. Closing Disclosure (CD) 3-day review window: federal law (TILA-RESPA Integrated Disclosure Rule) requires the buyer to receive the CD at least three business days before closing to confirm final cost itemization. Compare CD against the original Loan Estimate; any variance over $5K requires lender explanation. Sign closing documents: a notary witnesses the buyer signing 30-50 documents — Deed of Trust, Promissory Note, title transfer, various disclosures. Signing can happen at the title company office or via a mobile notary.

Wire down payment and closing costs: closing costs include transfer tax (roughly 0.11-0.15% of purchase price, with city-level supplements in some Bay Area municipalities), recording fee ($200-$500), title insurance (0.4-0.5% of purchase price), escrow fee ($1,500-$4,000), and prepaid property tax and insurance ($5K-$30K). On a $2M Bay Area home, total closing costs typically run $30K-$60K — on top of a $400K down payment, the wire total is $430K-$460K. Recording then escrow funded then keys: the title company submits the deed to the county recorder for registration (usually same-day), and once recorded, escrow releases funds to the seller and the buyer receives keys. Most Bay Area counties complete recording same-day, but Friday afternoon submissions can slip to Monday — so closing day should avoid Thursday and Friday when possible.

The 8-Phase Process Table

Headline numbers first: Bay Area home-buying from Phase 1 prep to Phase 8 keys typically runs 60-90 days. California defaults to a 17-day inspection contingency window, but mainstream Bay Area contested listings require the buyer to waive at offer. Earnest money runs 1-3% of purchase price (mainstream 3%); on a $2M home, total closing costs typically run $30K-$60K.

| Phase | Window | Key Actions | Typical Cost | Common Pitfall |

|---|---|---|---|---|

| 1. Pre-Approval | W -8 to W -4 | Compare 2-3 lenders, lock DTI math, run cross-border funds test wire | Pre-approval free; cross-border wire test $30-$50 | Skipping pre-approval to "see what's out there"; budgeting only the monthly payment |

| 2. Agent + BRA | W -4 to W -2 | Intro call, sign Buyer Representation Agreement (duration / scope / compensation) | Commission typically 2-3% of price (settled at closing) | First showing without signed BRA; signing too-long duration locks you in |

| 3. Search + Showings | W -2 to Day 0 | MLS + off-market + pre-market screening; cap at 15-20 showings | No direct cost | Past 25 showings, decision fatigue sets in; skipping online pre-screen wastes tour time |

| 4. Disclosure Diligence | Parallel to Phase 3 | TDS / SPQ / NHD review, pre-inspection, HOA docs, street-level school attendance lookup | Optional self-paid pre-inspection $400-$800 | Pushing disclosures to post-offer; using zip code instead of street-level for schools |

| 5. Offer Strategy | Day 0-3 | Price ladder, contingency calls, non-price levers, submit and counter | No direct cost | Using inspection contingency as negotiation lever; over-listing without modeling cash reserves |

| 6. Escrow Open | Day 3-7 | Open escrow, wire earnest money (1-3%), confirm inspection window | Earnest money 1-3% of price | Wire fraud (impersonation emails changing account info) |

| 7. Final Underwrite + Appraisal + Walk-Through | Day 14-25 | Loan underwrite, appraisal report, title insurance, final walk-through | Appraisal $700-$1,200; Title insurance 0.4-0.5% of price | Changing jobs or making big purchases mid-underwrite; no plan for low appraisal |

| 8. Closing + Recording | Day 25-30 | 3-day CD review, notary signing, wire balance, recording | Closing costs $30K-$60K on $2M; transfer tax 0.11-0.15% | Closing on Thursday or Friday and slipping; not reviewing CD line items |

The key takeaway from the table: Phase 5 (Offer) through Phase 8 (Closing) compresses to 25-30 days in the Bay Area — 1-2 weeks faster than most other states. The core driver is that Bay Area buyers routinely waive contingencies to simplify the contract. But that speed comes at a price: the buyer absorbs more risk. Waiving inspection contingency means latent structural defects fall to the buyer; waiving appraisal contingency means a low appraisal has to be covered with cash. The cost of Bay Area process speed is that buyer risk shifts earlier — into the quality of Phase 3-4 diligence. That is why this guide places disclosure review and street-level school verification alongside showings (Phase 3-4), not after escrow open (Phase 6).

MK Group Field Observations: Three Buyer Types, Three Different Processes

Cross-border entrepreneur families. These buyers need 30-60 days of front-loaded Phase 1 prep and run a completely different Phase 3 showing rhythm. In one Shenzhen entrepreneur engagement (referenced in the MK Group case library), the family contacted Marie in the morning and wanted to tour that same afternoon. Marie pulled four representative properties spanning Menlo Park, Palo Alto, Los Altos Hills, and Los Altos out of MLS and off-market inventory within 30 minutes, sequenced them deliberately cheapest to most expensive, and built the family a Silicon Valley luxury map in one half-day. The family did not bid on this trip but committed to returning when they were ready — the goal of a cross-border first tour is not to close that day; it is to build a judgment framework the buyer can operate from for months.

Cross-state AI families. MK Group recently served a Seattle dual-income AI scientist family with an 8-year-old daughter who relocated to Palo Alto in May 2026. Their Phase 1 was relatively simple (stable big-tech compensation), but Phase 3 had to be compressed 5x — every visit was a 3-5 day trip. The MK Group team pre-screened candidates remotely with walkthrough video and data filtering before the family flew in, so on-the-ground tour time concentrated on the 5-10 highest-match homes. Phase 2 agent selection added one extra dimension — remote responsiveness across Pacific time zones.

Local move-up families. The defining Phase 1 question is sequencing the sale of the current home against the purchase of the next. Three paths: sell first, then buy (cleanest financial position, but requires interim rental or rent-back), buy with a contingency (offer subject to current-home sale — sellers in contested Bay Area submarkets rarely accept this), or bridge loan (a short-term high-interest facility of $300K-$2M that funds in 2-3 weeks). Across Bay Area move-up families broadly, the most common path is sell-first plus a 2-3 month interim rental — the cleanest financial position. Bridge loans serve families unwilling to move twice. The simultaneous all-cash path is reserved for the small minority with the requisite liquidity.

Common Mistakes

Mistake 1: "Pre-approval and pre-qualification are basically the same"

Pre-qualification is a soft, self-reported, five-minute online estimate with no document review. Pre-approval is the hard commitment a loan officer issues after actually inspecting your W-2s, tax returns, bank statements, and credit report. Bay Area listing agents routinely reject offers attached only to pre-qualifications. The pre-approval letter — turned around within 24 hours by the right lender — is the document that gets you into the bidding pool.

Mistake 2: "The MLS shows me every property on the market"

The MLS is the publicly listed inventory, but Peninsula $5M+ off-market activity runs roughly 15-30% of inventory (MK Group industry-participant estimate, not MLS-sourced hard data), with the highest concentration in Atherton, Hillsborough, and Old Palo Alto. Off-market deals require agent-network access, which is one of the core reasons to select a well-networked agent. If you're only looking at Redfin and Zillow, you may be seeing only 70-85% of what's actually available.

Mistake 3: "Always keep the inspection contingency — it's the buyer's last line of defense"

The textbook logic is correct, but it doesn't survive a Bay Area bidding market. Sellers typically publish a pre-inspection report at offer review and expect buyers to waive the contingency outright; if your offer keeps the inspection contingency and then tries to use it to chip away at price, the listing agent usually pivots to the back-up offer instead of negotiating. The Bay Area middle path: pay $400-$800 for your own pre-inspection before submitting the offer, learn the risk profile, then choose to waive with eyes open. The buyer is buying information rather than holding a contingency as escape hatch.

Mistake 4: "Zip code 94027 means I'm in the Atherton school district"

Wrong. Atherton as a town spans three different elementary districts — Las Lomitas, Menlo Park City, and Redwood City — and elementary school assignment is determined street by street. MK Group worked an Atherton Oaks boundary diligence case where the buyer's first-choice home sat on the wrong side of the boundary; comparable homes one block over on the correct side were trading approximately $1.5M higher. Zip code does not equal school district, and city level is not granular enough — verification has to be at the street-level attendance area. Palo Alto Unified, Cupertino Union, and other Bay Area districts have similar boundary effects.

Mistake 5: "The pre-listing inspection report is enough — I don't need my own"

The seller's pre-inspection has structural bias: the seller chooses the inspector, the seller pays, and the seller controls how the report is presented. What buyers receive may be an edited version, and completeness of the reroof, HVAC, and major-system sections needs verification from the buyer's agent. The safest practice: pay for your own independent pre-inspection before submitting the offer and cross-check the two reports for consistency. This is why Bay Area pre-inspection culture has matured — both sides increasingly do their own.

Mistake 6: "On wire day, escrow emailed me a new account — I just updated and sent"

Wire fraud is the single most severe risk in the Bay Area buyer process. The common attack: hackers impersonate the escrow officer in email and provide "updated" wire instructions routing to a fraud account. Rule: any "account change" email must be verified by phone, calling escrow's main published number — never the number in the email body. A hacked down-payment wire ($500K-$2M+) is functionally unrecoverable. FBI IC3 data shows real estate wire fraud averages $200K+ in losses with under 30% recovery rates.

Next Steps

- Map the 8-phase windows backwards from your target closing date. Cross-border and cross-state buyers should start Phase 1 at least 90 days before target closing; local buyers, 60 days.

- Run 2-3 lender pre-approvals in parallel in Phase 1. Cross-border buyers run the small test wire at the same time — don't wait until you find the home to start.

- Sign the Buyer Representation Agreement before the first showing in Phase 2. Use the intro call to lock down the three dimensions (duration, scope, compensation) before signing — keep the duration short and renew if the working relationship is good.

- Run disclosure review and street-level school attendance verification alongside Phase 3 showings, not after the offer. The Bay Area cadence does not give you time to redo diligence after offer acceptance.

- Lock your price ceiling and contingency strategy with your agent before submitting the offer. Highest-and-best calls leave hours, not days, for six-figure decisions — those decisions are easier when the framework is already set.