The short answer

Yes. At the $10M+ tier, a buyer's agent's value is not "showing you the house." It is whole-chain risk anticipation — from area and off-market sourcing, through due diligence on hidden systems engineering, to loan structure and negotiation execution. In one real closing, a below-top offer carrying a roughly $10M loan won precisely on execution, beating all-cash rivals to be chosen by the seller.

This article is for decision-making education and is not legal or tax advice. Ownership structure (individual / LLC / trust), tax and succession planning, and cross-border funding should be confirmed with your attorney and CPA.

Who this article is for

If any of the following describes you, this article was written for you:

- You hold a $10M+ budget and plan to buy a long-term primary residence or long-hold estate in and around Atherton, Palo Alto, Los Altos Hills, Hillsborough, Woodside, or Saratoga;

- You have already toured a home through its listing agent and are weighing whether to bring in a second agent who represents only you;

- You are a cross-border buyer purchasing in the U.S. for the first time, still unfamiliar with off-market channels, jumbo financing, and ownership structure (individual / LLC / trust);

- Your criteria are already clear — quiet, private, a strong community, a home that holds its value — and you want to understand whether a buyer's agent still adds value in that situation.

Three dimensions that decide the question

To judge whether a buyer's agent is worth it, first get clear on what buyer representation actually does. At the $10M+ tier, the value concentrates in three dimensions — none of which is "opening the door for a showing."

Dimension one: information and access — can you even see the house?

In a top-tier market like Atherton, many of the genuinely great properties never appear in full on the public MLS. They move through long-standing relationships, market trust, and precise matching. Without access, you cannot even clear the first step of knowing which properties exist. A buyer's agent's first layer of value is opening the off-market and pocket-listing channels — placing you inside the pool of homes you will never find on Zillow. For how these channels work, start with Atherton Off-Market: How a Below-Top Offer Was Chosen Anyway · 中文.

Dimension two: due diligence and risk translation — can you read the house?

In a $10M+ home, much of the value is buried where you cannot see it: an underground equipment room and its heat-dissipation plan, built-in wiring and pre-run conduits, a three-tier independent doorbell and surveillance layout, lighting, security, and irrigation woven into one smart system — down to two full boxes of system manuals that stand for a decade of maintenance thinking. These details decide the home's real quality and its long-term cost of ownership, and a buyer is almost never able to identify them alone. A buyer's agent's second layer of value is translating the hidden engineering behind the paper terms, so you know exactly what you are paying for.

Dimension three: execution and negotiation — can you actually win the house?

Once you have found it and understood it, execution is what decides the outcome. Scarce top-tier estates draw multiple bidders, and the seller's criteria are sharper too — they want more than the highest price. They want certainty that the deal will close cleanly, and confidence that this buyer will truly understand and care for the home. A buyer's agent's third layer of value is anticipating every risk across the loan plan, the ownership structure, the negotiation rhythm, and the closing timeline — and hedging each one in advance, so your offer reads to the seller as the most certain and the best-fitting.

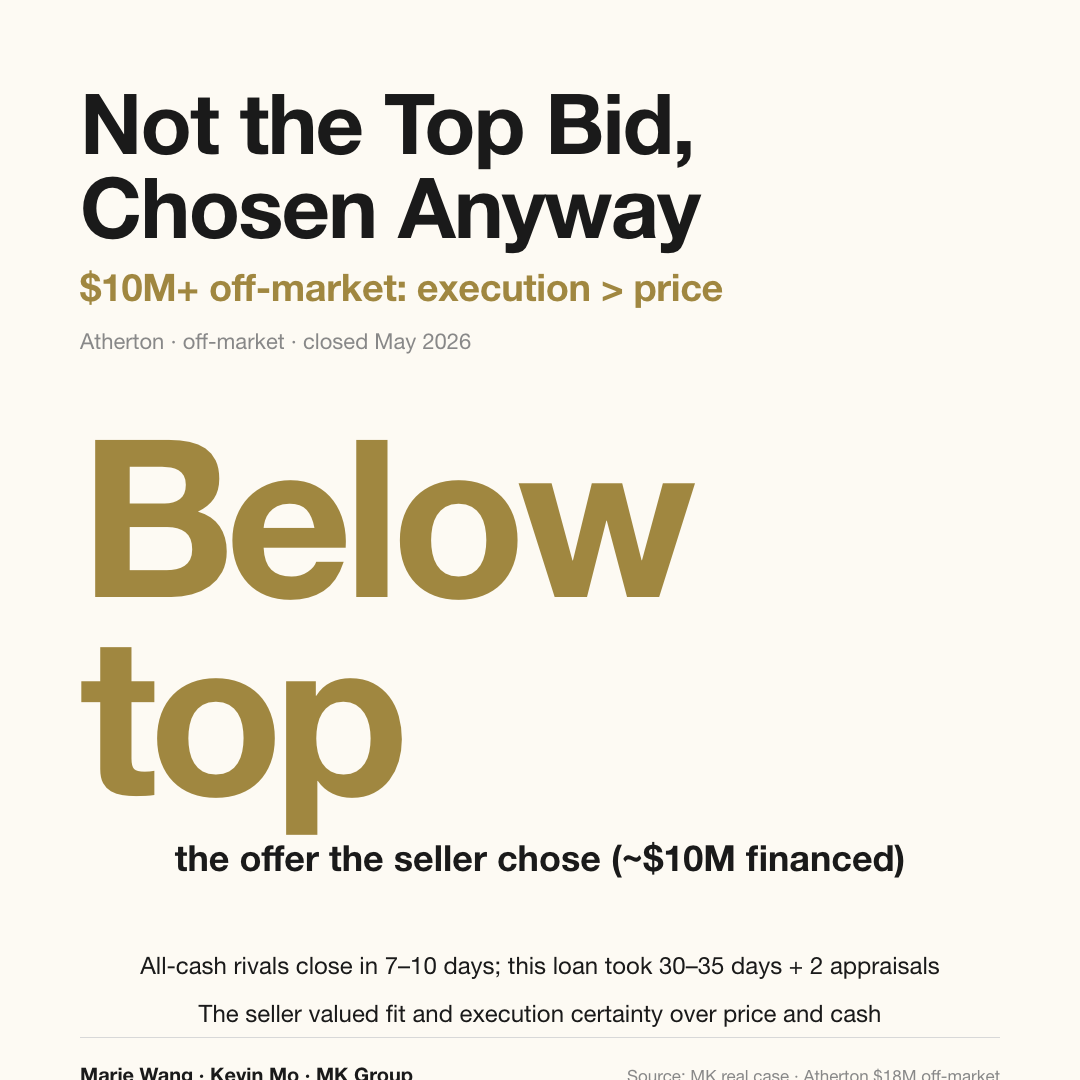

All-cash vs. financed: the certainty comparison

Start with the core numbers. At the $10M+ tier, an all-cash offer carries closing certainty of roughly 7–10 days with zero bank appraisals, while a buyer financing a roughly $10M jumbo loan needs about 30–35 days and two bank appraisals. Those extra three-plus weeks of uncertainty are the financed buyer's built-in disadvantage — and precisely what a buyer's agent has to hedge through execution.

| Item | All-cash buyer | Financed buyer (~$10M jumbo) |

|---|---|---|

| Typical closing period | ~7–10 days | ~30–35 days |

| Bank appraisals | 0 | 2 |

| Certainty from the seller's view | High | Must be built by the agent |

| Lenders able to fund this size | N/A | Few — lock early, run backups in parallel |

Data sources: real MK case (case-020, Atherton $18M off-market); NAR 2024 class-action settlement (public); MLSListings / MK Bay Area Pulse 2026 Q2

Updated: 2026-07

Scope: Bay Area Peninsula / South Bay $10M+ estate buyers

The counterintuitive point worth remembering: even though the financed buyer is clearly at a disadvantage on closing certainty, in one real Atherton off-market closing in May 2026, the buyer with a below-top offer carrying a roughly $10M loan still won. That tells you something about scarce top-tier estates: a seller's regard for fit and execution certainty can outweigh the surface advantages of price and cash — and building that certainty is exactly a buyer's agent's job. For market context: Atherton's 2026 Q2 median closing price was about $10.5M across 23 sales (source: MLSListings / MK Bay Area Pulse), and all-cash buyers are the norm rather than the exception at the Silicon Valley high end — which is precisely why the financed buyer needs professional execution to close the gap.

What MK Group has seen in practice

MK Group co-founders Marie Wang (DRE# 02110980) and Kevin Mo (DRE# 02127623) served as buyer's agents on an Atherton $18M off-market purchase that turned all three dimensions above into a single complete case. The home's original owner was an architect who spent four years building it by hand to his own living standard, with much of the value hidden in the equipment room, the built-in wiring, the three-tier surveillance, and the smart-system integration. The buyer was a cross-border client who had never purchased in the U.S. before and, for personal reasons, chose to carry a roughly $10M loan — while most rivals were all-cash buyers with real firepower.

The offer MK submitted was not the highest. But after meeting and talking with the buyer, the seller decided that same evening to accept it. Behind that decision was a full certainty program: introducing lenders able to fund a loan of this size and running several in parallel as backups; giving expert-level guidance on how to hold title (individual / entity / trust) and connecting the buyer to the right professionals; and, with a listing agent who was initially wary, putting the greatest share of the work into steady communication with the other side — "when they got nervous, we could not." The buyer even canceled trips to Japan and Korea and booked the first flight the next morning to see the home in person — a gesture of intent that became one of the turning points in the seller's re-evaluation. For a fuller breakdown of the loan-execution piece, see Financing $10M on an $18M Silicon Valley Estate Against an All-Cash Field · 中文.

A separate Saratoga $12M full buyer-representation case shows a different situation. The client's criteria were clear from the start — quiet, private, a good community, right for long-term living, with scarcity and a case for holding value. In this "clear criteria" scenario, sourcing the community and the property is actually the easier link; what really decides the outcome is the step-by-step anticipation and handling of risk across the whole chain — area screening → property judgment → pricing strategy → negotiation rhythm → inspection → closing timeline (one small complication along the way was resolved smoothly too). As MK puts it: "The right home is not necessarily the most expensive one on the market, but it is always the one best suited to the client's stage, family needs, and future plans." The two founders share more breakdowns of this kind on YouTube — @MarieWang (44K+) and @KevinMoRE (23K+).

Common misconceptions

Misconception one: "I already have a listing agent — why not just buy through them and skip a step?"

A listing agent's legal duty is to secure the best price and terms for the seller. If you buy directly through them, the best you can hope for is dual agency, where the representative's position carries a built-in conflict of interest — you can hardly expect the seller's agent to surface the home's hidden defects, argue for a reasonable price reduction, or fight for terms more favorable to you. Hiring an agent who represents only you is, at its core, putting someone on your side of the negotiating table.

Misconception two: "I have to pay the buyer's agent myself — so isn't it better to save it?"

Since the NAR class-action settlement took effect on August 17, 2024, buyers sign a written buyer-representation agreement before touring, and the buyer's agent's compensation is stated clearly and is negotiable — it is no longer posted uniformly through the MLS. That means compensation has become transparent, but "transparent" does not mean "should be cut." At the $10M+ tier, a single due-diligence blind spot or one negotiation misstep that a buyer's agent hedges away dwarfs the fee itself. Treat it as a negotiable, quantifiable risk-hedging expense, not a processing fee to trim wherever possible.

Misconception three: "My criteria are clear — I can find the house and write the offer myself."

Clear criteria only solve "what you want." They do not solve "how to win it." The Saratoga case above makes the point precisely: the clearer the criteria, the less the difficulty sits in community sourcing — it shifts to the back half of the process, the step-by-step risk anticipation across pricing strategy, negotiation rhythm, inspection, and the closing timeline. Scarce properties often draw multiple bidders, and without execution, even the clearest set of criteria can end up in someone else's hands.

Next steps

- Before touring your first home, sign a written buyer-representation agreement with an agent who represents only you, and settle the compensation terms up front — this is the standard process since the 2024 settlement, not an added burden.

- Assemble your "certainty profile": cash vs. loan, loan size, the timeline on funds you can deploy, and your target closing period — so your agent can design an offer structure that can compete with all-cash rivals.

- If you lean toward financing, lock in a lender able to fund at the jumbo size early and prepare several backups — do not start looking for money after you have found the home.

- Before writing an offer, consult professionals on how to hold title (individual / LLC / trust) and the corresponding tax and succession planning — especially as a cross-border buyer.

- Read a framework piece on how to choose an agent first to round out your evaluation criteria — for example, How to Choose a Bay Area Real Estate Agent — 8 Dimensions to Vet + a Decision Framework · 中文 — then interview two or three candidate buyer's agents against it.