The short answer

Yes — but at this price point it is an exercise in execution, not a contest of capital. Roughly 80% of Atherton closings are all-cash, and a $10M loan starts at a structural disadvantage: a 30–35-day timeline, two independent bank appraisals, and a very short list of lenders who will even write a check that size. Winning has never been about topping the price. It is about retiring every point of uncertainty before the seller has to worry about it. This article uses one real $18M off-market close to show how that is done.

Who this article is for

- Buyers who could pay cash but choose to finance. Families with the liquidity to close all-cash who would rather keep capital deployed elsewhere while still acquiring at the $10M+ tier.

- Cross-border families buying their first U.S. home. The principal is overseas, the house is on the Peninsula, and someone has to plan every step of an international close in advance.

- Financed buyers going head-to-head with cash. Bidders who want to know what certainty they can put on the table beyond simply raising the number.

- Buyers tracking the Atherton and Peninsula $10M+ off-market market. The best homes rarely reach a public listing; the deals happen inside relationships and trust.

- High-net-worth families who care about privacy and holding structure. People who treat the ownership vehicle — individual, LLC, or trust — as part of the transaction, not a patch applied after the fact.

Three decisions that actually settle the deal

Decision one: loan size determines whether a lender can even underwrite it

A $10M loan is not "a bigger mortgage." It is a different product. Most large banks can write an ordinary jumbo loan; almost none will underwrite an eight-figure one. That means you cannot rely on a single bank — if that one lender stalls at an appraisal or an underwriting step, the whole deal can unravel. The sound approach is to line up several lenders capable of that size before you write the offer, each with a backup ready to step in.

Decision two: timeline and appraisal milestones are where the disadvantage really lives

The soft spot in a financed structure is not "not enough money." It is time and uncertainty. A $10M loan typically needs a 30–35-day close and two separate bank appraisals — two banks each running their own independent valuation. An all-cash buyer, by contrast, can close in 7–10 days with zero appraisals. When a seller is already holding an offer that can fund in a week, the question in front of him is blunt: is three or four more weeks, and two more appraisals, worth it?

Decision three: the listing agent's trust is something you actively earn

In an off-market deal, the seller and the listing agent often start out not knowing you and not believing the deal will close. The buyer's agent's heaviest workload is frequently not with their own client — it is with the other side's agent. Steady, transparent, unflappable communication, with a solution placed in front of every problem before it hardens into a crisis, is what earns a below-top offer a serious hearing. This dimension, more than any other, decides whether a financed buyer can turn the disadvantage around.

Financed offer vs. all-cash offer: the structural contrast

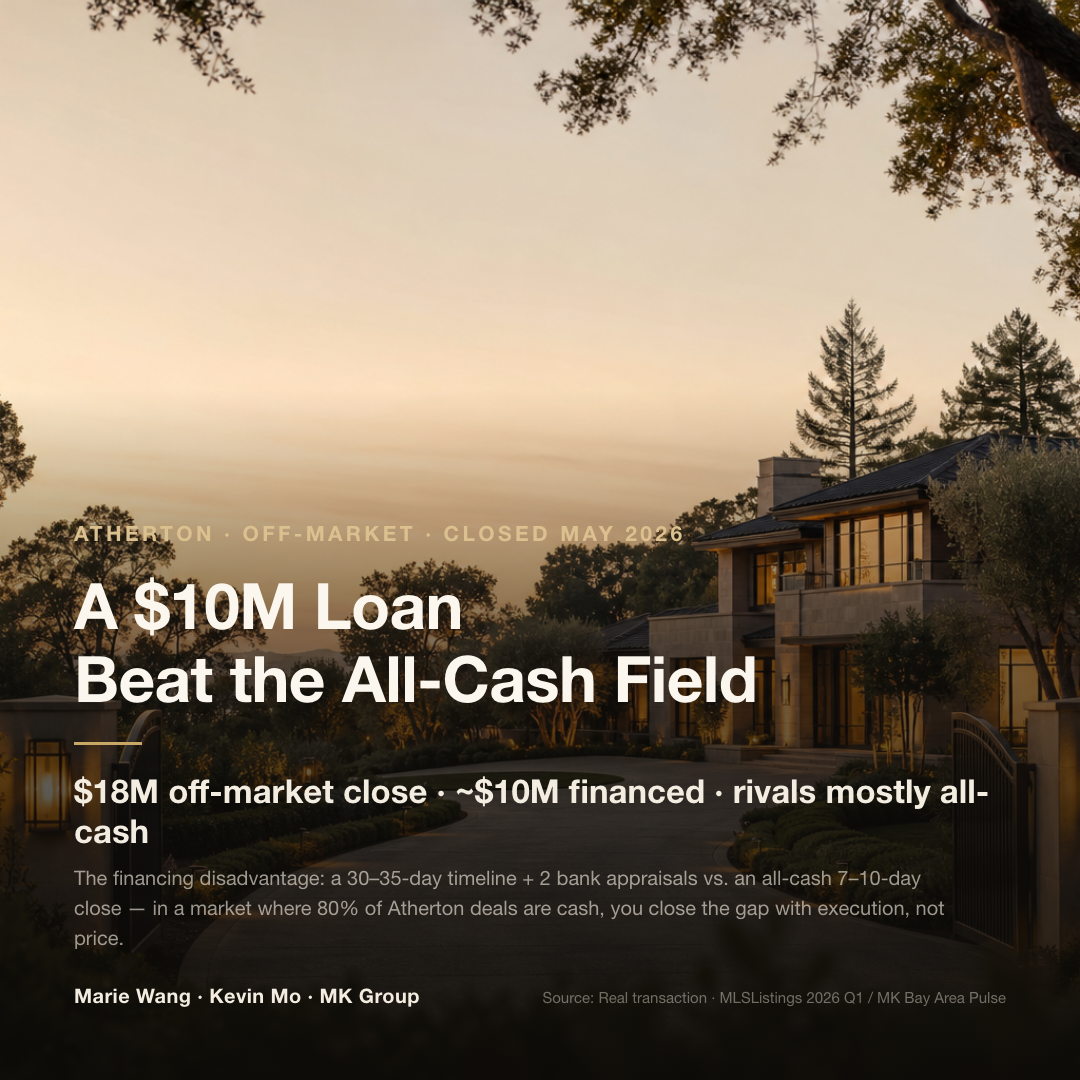

In the first quarter of 2026, Atherton recorded 10 residential sales at a median of about $15.71M, 80% of them all-cash, with a median of just 9 days on market. Across the wider Bay Area, of the 8 sales above $20M from January through mid-May 2026, only 1 carried a loan — all 6 that closed within Q1 itself were cash. An all-cash offer typically closes in 7–10 days with zero appraisals; a $10M loan needs 30–35 days and two bank appraisals. That gap in certainty — not the money — is what a financed buyer actually has to hedge.

| Dimension | All-cash offer | Financed offer ($10M tier) |

|---|---|---|

| Close timeline | ~7–10 days | 30–35 days |

| Bank appraisals | 0 | 2 (two banks, each valuing independently) |

| Who can underwrite | Not applicable | Very few lenders write this size |

| Certainty | High — funds in hand, ready to close | Depends on appraisal and underwriting milestones |

| Share of all Atherton closings | ~80% (2026 Q1) | ~20% |

What to remember: at this price point the financed buyer's disadvantage is not affordability — many of these buyers have the cash and simply choose to finance. The real disadvantage is the uncertainty that time and appraisals introduce. When a seller is simultaneously holding a buyer who can close in seven days, a 30–35-day offer that still has to clear two appraisals cannot buy back that certainty with price alone. You win it with execution — dismantling each uncertainty in advance until the seller can see that your path, though slower, will absolutely arrive.

What we saw on the ground

This transaction was the highest-priced of three eight-figure homes Marie Wang and Kevin Mo closed in May 2026 — an Atherton off-market estate that sold for $18M, where the buyer financed roughly $10M against a field of rivals who were mostly all-cash. The house had been built by its original owner, an architect, over four years to his own living standard, and much of its value sat in systems engineering you cannot see.

The difficulty was on the table from the first day. The buyer was overseas; the house had a queue of viewers lined up before it ever listed. MK toured it in person the next day, reported every detail back, and the buyer decided to make an offer on the spot. The seller declined it at first — a buyer who had never seen the house, needing a ~$10M loan, when he was not short of all-cash buyers with the means to close in a week. So the buyer canceled a set of planned trips to Japan and Korea, booked the next morning's first flight, and flew fifteen hours to see the house in person. That single act became the turning point in how the seller weighed the buyer's sincerity.

What followed was certainty, built one milestone at a time. A ~$10M loan is hard for ordinary banks and lenders to underwrite, so MK connected the buyer to a lender who could carry that size while running several lenders in parallel as backups — a fallback prepared at every step. The buyer had never purchased in the United States before, so MK effectively served as a full private concierge, planning each move in advance and giving expert-level guidance on how to hold title — as an individual, a company, or a trust — alongside succession planning, so the holding structure advanced in parallel with the loan and the close instead of slowing either one.

The largest share of the work, though, landed on the seller's side. The seller and the listing agent did not know MK at first, and did not trust that the deal would close. MK put the most effort into continuous communication with the other agent, holding steady under the triple pressure of the listing agent, the buyer, and the lender. In Marie's words, "When they panic, we can't panic." (Translated from Mandarin.) The team placed a solution in front of every problem, for every party. The house closed at $18M. Afterward, the listing agent wrote a long commendation letter to MK and to their manager — and has since begun working with MK on other high-value listings.

The deal closed, and price was almost beside the point. What made a financed offer the one the owner chose was the buyer's strong fit with the house, plus the execution that took apart every uncertainty ahead of time. For why a non-highest offer got chosen — and how the hidden systems-engineering value of a home like this is translated for a buyer — we broke it down in full in Atherton off-market: why the owner didn't take the highest offer. If your budget sits in the mainstream $2M–$5M band and you are also competing against cash, How to beat all-cash buyers in the Bay Area when you're financing covers tactics — pre-approval, condition compression — better suited to that tier.

Common misconceptions

"In an all-cash market like Atherton, a financed buyer has no shot."

The data is lopsided — Atherton was roughly 80% all-cash in 2026 Q1, and only 1 of the 8 Bay Area sales above $20M through mid-May carried a loan. But a low share is not the same as no chance. What a seller ultimately weighs is certainty, not the label "cash" itself. A financed offer with clean execution, a clear timeline, several lenders in reserve, and visible sincerity can absolutely beat a wishy-washy cash buyer. In this case the financed offer was not even the highest number, and the owner still chose it.

"If you're willing to bid higher, you can make up for a financed structure."

Raising the price closes a price gap; it does not close a certainty gap. The seller's worry is whether three or four more weeks, and two more appraisals, might go sideways — that is process risk, not a money problem. Rather than pouring the whole budget into the number, spend it on making the seller believe your path will finish: parallel lenders, a firm schedule, showing up in person, transparent communication. The marginal return on building certainty is usually higher than the last few hundred thousand of overbid.

"A $10M loan is just like any mortgage — find a big bank and you're set."

An eight-figure loan is another species. Very few institutions will underwrite one, and any single appraisal or underwriting snag can collapse the whole deal. The safe move is to approach several capable lenders in parallel before you write the offer, secure each one's pre-approval, and keep a backup. Going to look for the money only after the offer is accepted is the most dangerous sequence at this price.

"You can sort out the holding structure after the deal closes."

Whether you hold as an individual, a company, or a trust touches privacy, tax, and succession, and is best settled with your attorney and CPA at the same time you write the offer — running in parallel with the loan and the close. At this price, clients usually care about far more than the purchase itself: the whole process, their privacy, and the ownership structure. Leaving the structure for last tends to become the very thing that slows the close.

Next steps

- Lock the money before you offer. Approach 2–3 lenders who can underwrite your loan size in parallel, get each one's pre-approval and a backup, rather than hunting for financing after the offer is accepted.

- Write certainty into the offer. Spell out the close timeline and the appraisal milestones in your schedule, and proactively show the listing agent that every step on your side is controlled — instead of leaving them to guess whether the loan will drag.

- Arrange an in-person showing early. If you are overseas and the house is on the Peninsula, it is worth showing up in person even on a tight schedule. Presence weighs far more in a seller's read of your sincerity than an online bid.

- Run the holding structure in parallel. Settle individual / company / trust ownership with your attorney and CPA at the same time you write the offer, so title planning never becomes the step that slows the deal.

- Treat the listing agent as your second client. Proactive, transparent, steady communication is often the deciding factor in whether a below-top offer gets chosen.