The short answer

Yes, you can win. In the $2M–$5M tier across the Peninsula and Silicon Valley, the real reason financed buyers lose to all-cash rivals usually isn't a lower price — it's an offer that drags, loan terms that read as uncertain, and a slow decision. What a seller fears most is not that you bid a little under; it's whether your offer might fall apart. Bring your decision speed and offer certainty up to parity with the cash buyers, and you can win even when the money isn't equal — as long as you first understand exactly how many cash buyers you're actually up against.

Who this article is for

This is written for one very specific reader. You're a tech family on the Peninsula or in Silicon Valley with a meaningful down payment and steady income, shopping in the $2M–$5M tier and getting ready to write an offer — but you're not paying cash, you need a mortgage. You've heard an agent at an open house say "this one already has a few all-cash offers," and you've started to wonder whether you ever had a shot.

If you're about to bid on a particular home, want to know exactly how much competitive pressure you're under, and want to know what else you can do short of bidding endlessly higher, this article is for you. We're not going to profile who the cash buyers are — that's a different piece — we're going to answer one thing: how a financed buyer wins.

Three dimensions to judge first

Before you agonize over whether to add another 1%, locate yourself on three dimensions. They tell you where to spend your effort.

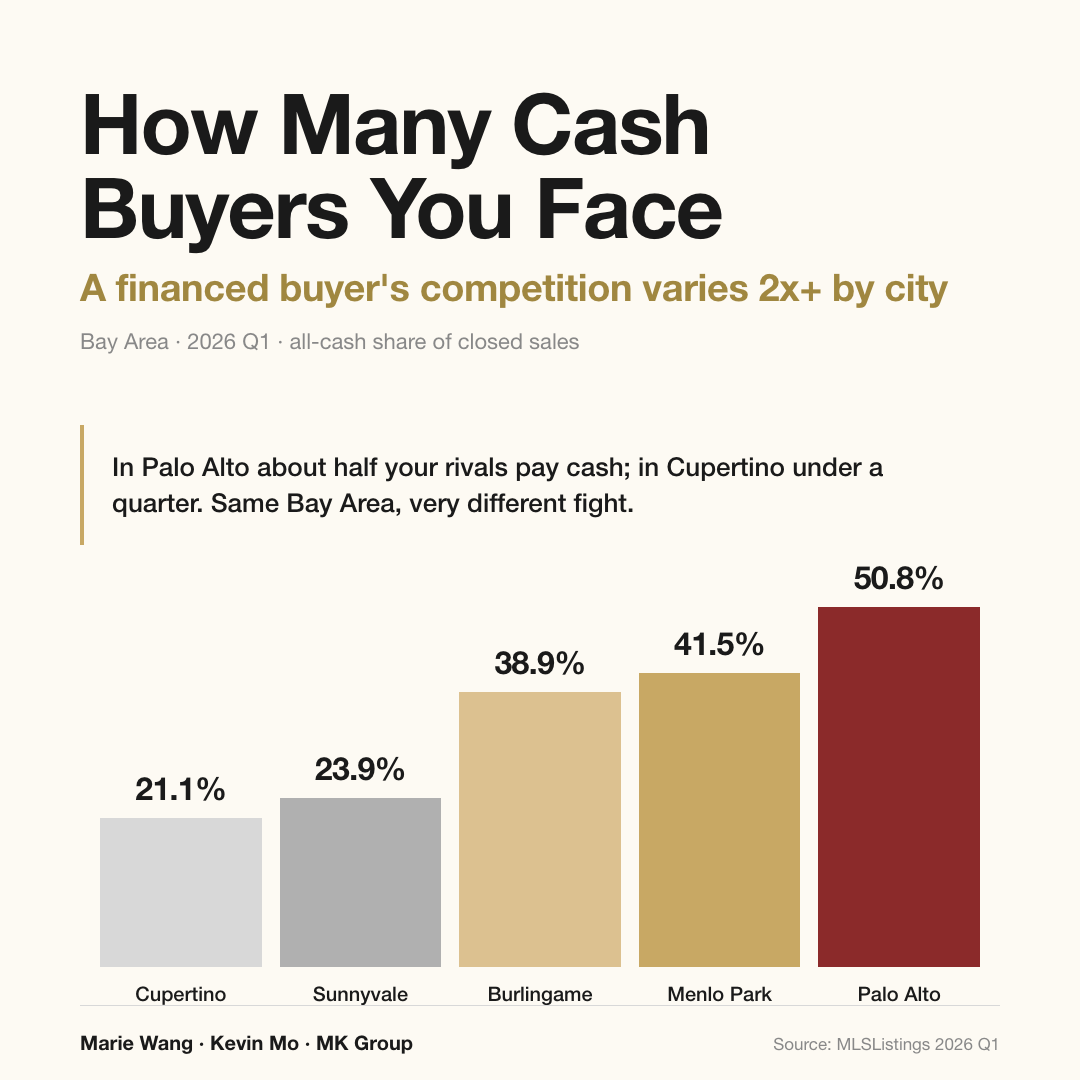

One: how dense the cash competition is in your city. This is the first number to know before you write anything. In Palo Alto, 50.8% of Q1 2026 closings were all-cash — so it's roughly a coin flip whether the person across the table needs a loan. In Cupertino that share is only 21.1%; about one in five of your rivals pays cash. Different cities, completely different intensity, and the playbook should differ with it.

Two: whether you're chasing a scarce, benchmark home. Within the same city, a scarce home that draws multiple offers on listing day and a home that's sat for three weeks follow opposite logic. For the first, you max out speed and certainty; for the second, you actually have room to negotiate terms. You have to grade the scarcity on listing day — not drive home and think it over. This is where financed buyers most often lose.

Three: whether your offer is clean enough on certainty. Sellers aren't comparing two numbers; they're comparing which offer is more likely to close smoothly. How far your loan approval has progressed, whether you carry a loan contingency, and what happens if the appraisal comes in low — those three things decide whether the seller reads your offer as "solid" or "shaky." Cash buyers hold a natural edge on all three, but a financed buyer can close that gap to near zero with front-loaded diligence.

Cash share by city: how many cash buyers you're really up against

The core numbers first. Among real Q1 2026 closings, the all-cash share was 50.8% in Palo Alto, 41.5% in Menlo Park, 38.9% in Burlingame, and 37.0% in San Mateo, then dropped to 23.9% in Sunnyvale and just 21.1% in Cupertino (source: MLSListings Q1 2026). Put plainly: in Palo Alto you have roughly even odds of running straight into an all-cash rival, while in Cupertino that probability is under one in four. Same "Bay Area," more than double the difference in intensity.

| City | All-cash share | Median sale price | Median days on market |

|---|---|---|---|

| Palo Alto | 50.8% | $4.12M | 8 days |

| Menlo Park | 41.5% | $3.40M | 7 days |

| Burlingame | 38.9% | $3.205M | 9 days |

| San Mateo | 37.0% | $2.30M | 7 days |

| Mountain View | 28.6% | $2.834M | 7 days |

| Los Altos | 28.0% | $5.082M | 8 days |

| Sunnyvale | 23.9% | $2.70M | 8 days |

| Cupertino | 21.1% | $3.43M | 7 days |

Two differences are worth remembering. First, the pricier the city, the denser the cash competition — Palo Alto, Menlo Park, and Burlingame, all three with $3M+ medians, sit above 38% cash, while engineer-dense cities like Sunnyvale and Cupertino, where buyers assemble RSUs plus a mortgage, run clearly lower, and a financed buyer's relative disadvantage there is much smaller. Second, the median days on market across the eight cities clusters at 7–9 days (most at 7–8, with the slowest, Burlingame, at just 9) — meaning that regardless of how high the cash share runs, these homes sell extremely fast, and a half-step too slow knocks you out. Speed is the problem a financed buyer has to solve even more than a cash buyer does.

There's also a ladder that's easy to miss: cash share climbs steeply as price rises. In Q1 2026, the all-cash share was 29.1% in the $3M–$5M band and jumped to 53.7% in the $5M–$10M band (source: MLSListings Q1 2026). That's exactly why this article is anchored to the $2M–$5M tier — at this level most of your rivals are not paying cash, and your financed status hurts you far less than you'd imagine; once you move above $5M, cash truly becomes the norm. To see how each city's over-asking premium corroborates this pace, read How Much Over Asking Do You Need to Win in the Bay Area? 2026 Q1 Premium by City.

Data source: MLSListings (Q1 2026 closings by city and price band, including all-cash share, median price, and median DOM); Freddie Mac PMMS via FRED (30-year fixed rate 6.11%, average across Q1 2026)

Updated: 2026-06

Scope: Peninsula and Silicon Valley single-family homes in the $2M–$5M tier, from the financed buyer's perspective

What we see in the field

Start with a counterintuitive real case. MK Group worked with a buyer carrying a $10M budget, 100% all-cash, shopping in Palo Alto. The interiors, materials, and renovation quality all met expectations. After the showing, the buyer wanted to "go home and think about it for one night" — by their experience in the mid tier, a $10M home shouldn't draw an instant rival. By the next morning the home was in contract, taken by another buyer. The buyer's first reaction: "Even a $10M home moves this fast?"

The lesson cuts deep precisely because even an all-cash buyer can lose by being slow. If cash can't save a slow decision, the takeaway for a financed buyer is sharper still — you're naturally a step behind on the approval process, so the only move is to front-load every piece of diligence you can and compress the time from "saw the home" to "can sign the offer" to the minimum. The line Marie Wang (DRE# 02110980) and Kevin Mo (DRE# 02127623) come back to in client debriefs: the scarcity assessment has to be done on listing day, because "let me sleep on it" is a dangerous move in a core spring market.

The other side: financed and equity buyers do close in this tier, and they close on solid ground. MK Group worked with a senior engineer who had spent 11 years at Applied Materials and completed an upgrade purchase funded by years of accumulated RSU vesting, landing in the Los Altos / Cupertino area. He wasn't a founder, wasn't an all-cash buyer — he was an engineer who had kept his head down at the same "shovel company" for years. On the day he signed, he told Kevin: "I just caught a good moment." In Q1 2026, Santa Clara County's overall average price was down 1.6% year over year, yet $5M+ closing volume was up 115% year over year — he is exactly the kind of buyer pushing that curve. The point: in the $2M–$5M tier, financed and equity-structured tech buyers aren't a fringe group, they're the genuine bulk of closings. Your job isn't to become a cash buyer — it's to polish a financed offer until the seller trusts it.

Common mistakes

Mistake 1: "An all-cash offer always wins, and as a financed buyer I have no shot"

Wrong. Sellers don't choose offers on the "cash vs. loan" label — they choose on which offer is most likely to close cleanly. A financed offer with the loan contingency already removed, an appraisal-gap clause as backstop, and the ability to close within 21 days can read nearly as certain to a seller as all-cash. And the real case above proves it cuts both ways: even an all-cash buyer lost a home to a slow decision — cash is never a get-out-of-jail card. In the $2M–$5M tier, most cities aren't even majority-cash (Cupertino 21.1%, Sunnyvale 23.9%, source MLSListings Q1 2026), so a sizable share of your rivals are financed buyers just like you.

Mistake 2: "To win I have to outbid the cash rivals by 1–2%"

This is the most common — and most expensive — mistake financed buyers make. In a market where median days on market is just 7–8 days, adding 1–2% does far less than "deciding a day faster plus a more certain offer." The all-cash buyer above didn't lose on a low bid; he lost by thinking it over one extra night. Spending your budget on shortening the loan contingency, backstopping with an appraisal gap, and finishing proof of funds early moves a seller more than a higher number — because you're solving what the seller actually worries about ("will this fall through?") rather than "will I net a little less?"

Mistake 3: "A pre-approval means my money is ready"

A pre-approval is only a preliminary indication a lender issues based on your self-reported information — it's a distance from "the money is certain," and sellers know that too. What actually makes a financed offer look like cash is a pre-underwrite: the lender has already verified your income, assets, and credit, with only the specific property and appraisal left to lock in. Carrying a pre-underwrite rather than a pre-approval is a financed buyer's first step toward real offer certainty, and the key move for pulling level with cash rivals.

Mistake 4: "The loan contingency protects me — I can never drop it"

The loan contingency is genuine buyer protection, but in a multiple-offer fight a seller reads it as risk. The right move isn't to remove it blindly — it's to first drive your loan risk to near zero with a pre-underwrite, then compress the contingency window on that basis (say, from 21 days to 7–10), and remove it only where the risk is controlled; meanwhile use an appraisal-gap clause to spell out "if the valuation comes in short, here's how much cash I'll cover," hedging the seller's biggest fear — a low appraisal — separately. It's a combination, not the isolated act of "deleting a clause."

Next steps

- Upgrade from pre-approval to pre-underwrite first. Have the lender actually verify your income, assets, and credit, and hold the pre-underwrite result — the first step in making a financed offer look like cash, and something to finish before you write any offer.

- Check the cash density in your target city. Use the per-city cash shares above: in Palo Alto (50.8%) you max out speed and certainty; in Cupertino (21.1%) your financed status hurts far less, so your effort goes elsewhere.

- Grade scarcity on listing day — don't drive home and think. The day you see the home, judge its scarcity against comparable competition over the past 12 months and decide whether to attack at full speed or negotiate on terms — even an all-cash buyer has lost a home to "let me sleep on it."

- Design for certainty, not just a higher price. Use a pre-underwrite to support shortening or removing the loan contingency, pair it with an appraisal-gap clause to hedge the valuation gap, and solve the seller's biggest fear — "will this fall through?" — up front.

- Anchor the rate cost into your full budget before you price. The Q1 2026 30-year fixed rate was about 6.11% (source: Freddie Mac PMMS); compute your real monthly payment and carrying cost off your actual down payment and loan amount, then set your offer ceiling — that's how your bids stay bounded instead of led by emotion. For a systematic look at offer structure and clause design, read Bay Area Buyer Negotiation in Practice: Offer Structure, Clause Design, and Raising Your Win Rate; to understand why the cash-buyer pool is so large, read Are 48% of Silicon Valley Buyers All-Cash? Who's Holding Up Bay Area Prices.