Direct Answer: How Bay Area Off-Market Luxury Listings Actually Trade

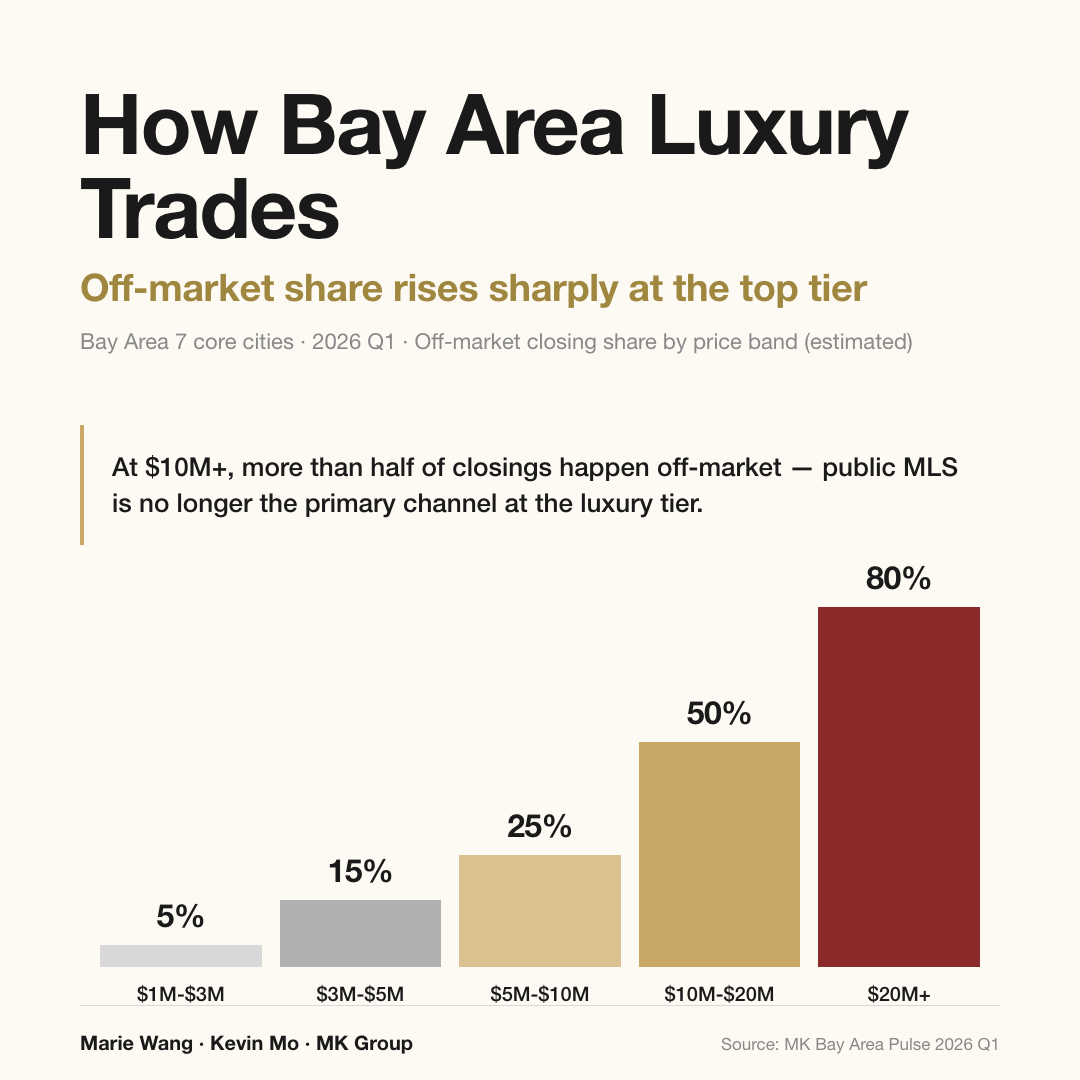

Bay Area off-market listings (also called pocket listings, private listings, or whisper listings) rise sharply in share at the $5M+ tier. Five core facts must be understood up front: (1) Off-market share scales with price band — roughly 5% at $1M-$3M, 15% at $3M-$5M, 25% at $5M-$10M, 50% at $10M-$20M, and 80% at $20M+ per MK Bay Area Pulse 2026 Q1 estimates. (2) Since MLS Clear Cooperation Policy took effect in 2020, true off-market must be an "office exclusive" — zero public marketing, no MLS, no Zillow, no social media; any "we'll preview internally for 7 days then list on MLS" coming-soon flow no longer qualifies as off-market (that's MLS pre-launch). (3) Three-layer channel architecture — brokerage-internal pre-MLS pools (Compass Private Exclusives and Sotheby's private networks as industry reference cases), agent-to-agent networks (Top Agent Network and similar membership-gated circles), and personal broker relationships (the private mailing lists and direct-dial relationships local luxury agents build over 5-20 years in a sub-market). (4) Off-market is the norm in Atherton — public MLS is the minority channel; the $15M+ tier runs 85-95% off-market and $20M+ approaches 100%. (5) Buyers enter the off-market pool through broker dealflow, not brand-name affiliation; sellers choose off-market primarily for privacy and price control. This is the framework Marie Wang and Kevin Mo at MK Group have refined across multiple Atherton, Palo Alto, and Los Altos Hills luxury engagements.

Who this article is for

This guide is written for five reader profiles:

- Cross-border high-net-worth buyers — from mainland China, Singapore, Hong Kong, and Taiwan, targeting $5M-$30M+ Bay Area luxury homes within compressed 14-30 day tour windows, where typically 80%+ of real dealflow at the upper tiers is not on MLS.

- Family offices — deploying capital for long-term Bay Area positioning, targeting $10M-$30M+ estate-grade assets, sensitive to privacy and wanting access to Atherton, Hillsborough, and Los Altos Hills inner circles.

- Privacy-sensitive sellers — well-known families, public-company executives, cross-border entrepreneurs, AI company founders — who don't want Zillow showing neighbors their home is on the market and don't want closing prices permanently public.

- Pre-IPO or secondary-market liquidity sellers — selling property in the window around a public listing, motivated by reputation management or tax planning, unwilling to list openly.

- Atherton, Palo Alto, and Los Altos Hills buyers — who have already chosen a tier but don't understand why "only three Zillow listings show up" — because the other 7-10 sit in the off-market channel.

Whichever profile applies, understanding how off-market actually operates is a prerequisite for effective $5M+ deployment.

What Off-Market / Pocket Listing Actually Means — Definition, Compliance, Differences from Public MLS

"Off-market," "pocket listing," "private listing," and "whisper listing" are used interchangeably in the industry. The core definition: the listing does not enter the MLS (Multiple Listing Service) public database, does not appear on Zillow / Redfin / Realtor.com, and carries no public marketing (no social media advertising, no Open House, no yard sign).

In May 2020, the NAR MLS Clear Cooperation Policy (CCP) took full effect and reshaped the compliance perimeter for pocket listings. The core CCP requirement: once a listing agent does any "public marketing" outside of MLS — including yard signs, social media posts, coming-soon stickers, email blasts to broader networks — the listing must be entered into MLS within one business day. This means the pre-2020 workflow of "preview in our office for 30 days plus run social media ads plus put up a yard sign" is no longer compliant — any public promotion forces an MLS listing.

After CCP, true off-market collapses to one compliant form: "office exclusive" — the listing stays entirely within the listing brokerage, with zero external public marketing (no yard sign, no social media, no Zillow, no broker preview emails beyond the MLS-internal universe). The seller must sign a written exclusion authorization explicitly opting out of MLS entry. Office exclusive is the only post-CCP compliant off-market form.

Several commonly confused concepts must be separated:

- "Coming Soon" listing (MLS Coming Soon status) — the listing is already in the MLS database with status "Coming Soon" and typically converts to Active after 7-21 days. This is not off-market; this is MLS pre-launch. Buyers can see the listing on Zillow and Redfin; they just can't submit offers yet.

- "Pre-MLS" / "Pre-Market" — same idea, usually referring to the broker preview window before MLS listing, but as soon as the listing agent does any public marketing, MLS entry is required.

- "Office Exclusive" — the true CCP-compliant off-market form — zero public marketing, flowing only within the brokerage and trusted private networks, requiring written seller authorization.

- "Pocket Listing" — industry shorthand, usually synonymous with office exclusive, but the compliance perimeter depends on whether the listing agent strictly observes the "zero public marketing" line.

How to tell whether a supposedly "off-market" listing is actually compliant: check whether the listing agent has posted on social media, used a yard sign, or emailed a broader broker preview list (targeted emails to specific buy-side brokers are fine; mass mailings are not). This matters for buyers — if the listing agent is operating out of compliance, NAR or state association review during your transaction can force the listing back into MLS and disrupt your deal.

Real Bay Area Off-Market Share Data — Broken Out by Price Band and by City

The headline numbers up front: Bay Area off-market share scales with price band — roughly 5% at $1M-$3M, climbing to roughly 50% at $10M-$20M and 80% at $20M+. Broken out by city, Atherton runs 50-95% off-market town-wide and public MLS is the minority channel; Palo Alto runs 25-40% off-market and remains predominantly MLS-driven. The combination means that even at "luxury" tier, Atherton and Palo Alto require completely different buy-side strategies.

| Price Band | Off-Market Share (Estimated) | Typical City Distribution | Primary Channels |

|---|---|---|---|

| $1M-$3M | ~5% | Bay Area-wide (South Bay dominant) | Limited office exclusive; predominantly MLS |

| $3M-$5M | ~15% | Cupertino / Los Altos / Mountain View / Sunnyvale upper tier | Brokerage-internal early signals + limited office exclusive |

| $5M-$10M | ~25% | Palo Alto / Los Altos / Menlo Park / Atherton entry | Brokerage pre-MLS pool + TAN agent-to-agent + personal broker relationships |

| $10M-$20M | ~50% | Atherton / Hillsborough / Los Altos Hills / Palo Alto upper tier | TAN + Compass Private Exclusives / Sotheby's private + personal broker relationships |

| $20M+ | ~80% | Atherton / Hillsborough / Woodside trophy estates | Personal broker relationships + ground-up builder direct + family-circle introductions |

The shift worth remembering: from the 5% off-market share at $1M-$3M to roughly 80% at $20M+, share grows 16-fold. $10M+ is the inflection point — once your budget crosses that line, watching MLS alone forfeits access to half or more of the inventory.

By city (2026 Q1 estimates, $5M+ tier):

- Atherton: 50-95% off-market (share rises with tier; $15M+ runs 85-95% and $20M+ approaches 100%). Atherton is the most extreme off-market city in the Bay Area — driven by the 1-acre minimum zoning, the town's zero commercial activity, and the resident base's acute privacy preference.

- Hillsborough: 40-70% off-market. The most privacy-focused luxury tier in San Mateo County, with $10M+ estates concentrated across Lower, Upper, and Country Club Manor sub-markets — sharing Atherton's "quiet legacy wealth" culture.

- Woodside: 40-60% off-market. Lots typically 1-5 acres with strong equestrian character, sellers and buyers both privacy-sensitive, market velocity slower than Atherton (60-180 day closing cadence).

- Los Altos Hills: 35-55% off-market. Primary $8M-$25M luxury city with substantial MLS inventory still active, but off-market share is rising at the trophy-estate tier.

- Palo Alto: 25-40% off-market. Even at $10M+, Palo Alto remains predominantly MLS-driven — a meaningful contrast to Atherton, tied to PAUSD school-district-driven buyer pool breadth (district families continue to source predominantly via MLS).

- Menlo Park: 20-35% off-market. $5M-$10M tier still predominantly MLS; off-market share rises in the $10M+ band.

- Los Altos: 15-30% off-market. $5M-$8M tier predominantly MLS; limited off-market activity at the trophy-estate tier.

Data sources: MK Bay Area Pulse 2026 Q1 field observation + MLSListings public closing records + Top Agent Network share data (per-brokerage internal statistics). Important caveat: off-market share is not an MLS-published fact — by definition off-market listings are absent from the MLS database, so all share figures are reverse-estimates based on industry observation plus known off-market closings; actual share may vary 5-10 percentage points either direction. Updated: 2026-06. Scope: 7 core Bay Area cities (Atherton, Hillsborough, Woodside, Los Altos Hills, Palo Alto, Menlo Park, Los Altos), $5M+ luxury tier off-market share and channel architecture.

The Three-Layer Off-Market Channel Architecture — Brokerage / Agent-to-Agent / Personal Broker Relationships

True off-market flow is not a black box of "seller → broker → mystery buyer" — it has a clear three-layer architecture. Understanding these three layers is the key to judging whether your broker actually has dealflow access.

Layer 1: Brokerage-internal pre-MLS pools. Every leading luxury brokerage runs an internal "pre-listing" pool — the listing agent shares the listing inside the brokerage after the listing agreement is signed but before MLS entry. The two most-cited industry examples: Compass Private Exclusives is Compass brokerage's internal off-market pool, accessible to Compass-affiliated agents who can preview listings before MLS entry; Sotheby's International Realty private networks are Sotheby's global brokerage's internal luxury off-market flow system, especially active at the $5M+ tier. These are industry reference cases — other large luxury brokerages (Keller Williams, Coldwell Banker Global Luxury, Christie's International Real Estate, Berkshire Hathaway HomeServices) operate their own internal pre-MLS pools with brokerage-specific names, rules, and coverage. Key constraint: under CCP, brokerage-internal pre-MLS pools can only function as a short-term warm-up channel (typically 7-21 days); if the seller chooses true "office exclusive" with no MLS entry, a written exclusion is required. The gate for buyers entering this layer: your buy-side broker must work at that brokerage or be inside the partner-brokerage circle.

Layer 2: Agent-to-agent networks (membership-gated circles). This is the cross-brokerage off-market flow channel, anchored by Top Agent Network (TAN) — membership based on closing volume (typically top 10% of local agents) plus referrals; members share listings (off-market and pre-MLS) with one another. The Bay Area has comparable circles including The Realty Alliance. The logic of these membership-gated circles: closing-volume thresholds filter out low-quality agents, referrals secure trust, and members share off-market listings on a "give one to get one" reciprocity that compounds over time. The gate for buyers: your buy-side broker must be a TAN (or comparable) member. This matters — the brokerage name on a business card does not signal TAN membership; ask directly, "Are you a TAN member?" and verify on the TAN website.

Layer 3: Personal broker relationships (private mailing lists / direct dial). This is the most opaque and highest-quality layer — local luxury agents working Atherton, Hillsborough, Woodside, and Los Altos Hills for 10-20 years accumulate 50-200 person private mailing lists or direct-dial relationships. These relationships include local listing agent peers, multi-generational estate owner families, ground-up builder teams (Pacific Peninsula Group, Devcon, Pacific Coast Land Design / Build, Conrad, Klopf, etc.), estate attorneys, family CPAs, and wealth managers. In the $15M-$30M+ tier, many listings never enter Layer 1 or Layer 2 — they flow entirely inside this layer of personal relationships. This layer is impossible to assess from credentials or affiliations; you can only evaluate it from "actual closing volume in the sub-market over the past 5-10 years" plus peer-reputation references. The gate for buyers: your buy-side broker must have 5-10 years of actual closing experience in Atherton, Hillsborough, or Los Altos Hills at the relevant tier, and standing among the local luxury broker peer group.

Coverage differs across the three layers: Layer 1 (brokerage-internal) covers roughly 30-40% of off-market listings; Layer 2 (agent-to-agent) roughly 30-40%; Layer 3 (personal broker relationships) covers 50-70% at the $15M+ tier — which is why the $20M+ off-market share reaches 80% and is essentially "uncrackable on your own." Marie Wang and Kevin Mo at MK Group operate across all three layers; in the half-day curated luxury tours used for cross-border buyers, a meaningful share of the homes shown come from the overlapping output of these three layers — which is how dealflow actually works in Atherton, Palo Alto, and Los Altos Hills.

How Buyers Enter the Off-Market Pool — 5 Real Channels

The gate for buyer access to the off-market pool is not budget — it's whether the broker has real dealflow. Five concrete channels:

Channel 1: Choose a broker with real dealflow, not just a brand name. This is the most important step. Diagnostic criteria: (a) How many actual closings has your buy-side broker completed at the target city and tier (Atherton, Palo Alto, Hillsborough) over the past 24 months? Fewer than 3 is insufficient. (b) Is the broker a Top Agent Network or comparable membership-gated circle member? Verifiable directly on the TAN website. (c) Can the broker deliver, within 7 days of intake, a "current off-market shortlist matching your profile"? This is the hard test of real dealflow — talk-only brokers cannot; brokers with actual circles can produce one within a week. The MK Group intake process in Atherton, Palo Alto, and Los Altos Hills uses this 7-day shortlist delivery as a standard diagnostic.

Channel 2: Leverage your broker's brokerage pre-MLS pool. If your broker works at a leading luxury brokerage (Compass, Sotheby's, Keller Williams, Coldwell Banker Global Luxury), the broker can give you access to the brokerage-internal pre-MLS pool. Specific approach: have your broker enter your buyer profile (budget, target cities, square footage, other preferences) into the brokerage's internal "buyer needs" system, so listing agents preparing pre-MLS listings see matching buyer profiles first and contact your broker directly. This layer is most effective in the $5M-$15M band.

Channel 3: Access via Top Agent Network and comparable membership circles. TAN is the most established cross-brokerage off-market sharing circle in the industry, with membership based on closing volume plus referrals. If your broker is a TAN member, the broker can search active off-market listings on the TAN platform or send a "buyer needs" email to the full membership. This layer is most effective in the $10M-$25M band. Verification: ask your broker to show you a TAN platform screenshot of current active off-market listings, or to walk through closings completed via TAN over the past 6 months.

Channel 4: Local luxury broker personal networks. This is the dominant channel at the $15M+ tier — many listings never reach Layer 1 or Layer 2, flowing directly through private mailing lists and direct-dial relationships among local luxury agents. To enter this layer, your broker must have 5-10 years of actual closing experience at the target city and tier and standing among the local luxury broker peer group. Diagnostic: can the broker, at intake, name at least 5 other top brokers in that city and walk through recent off-market deals completed in collaboration with them?

Channel 5: Direct outreach from sellers or listing agents. The rarest but occasionally effective channel — some sellers or listing agents reach out directly to a known high-quality buyer pool (often via wealth manager, estate attorney, or family office introductions) proposing an off-market deal. This layer cannot be actively triggered, only "passively surfaced" — by ensuring your wealth manager and estate attorney know you're searching for a $10M+ Atherton estate, so that if one of their clients sells, the introduction can be made. MK Group occasional scenario: a cross-border family office client's family attorney also represents an Atherton seller and brokers an off-market deal directly.

Channel weighting: $5M-$10M relies primarily on Channels 1 and 2; $10M-$20M shifts to Channels 1 and 3; $20M+ relies primarily on Channels 4 and 5. The higher the budget, the more critical the depth of the buy-side broker's relationships. This section covers cross-border capital compliance and trust ownership structures; please confirm execution details with your collaborating attorney or CPA.

When Sellers Choose Off-Market — 5 Real Reasons

Sellers don't choose off-market because they "can't find a buyer" — they choose it based on specific strategic objectives. Five real reasons:

Reason 1: Privacy. The most common reason at the $10M+ tier — well-known families, public-company executives, cross-border entrepreneurs, AI / tech company founders — none of whom want Zillow showing neighbors their home is on the market, none of whom want high-resolution estate photography circulating on social media, and none of whom want closing prices permanently public (MLS closing prices remain visible on Zillow and Redfin indefinitely). In Atherton, Hillsborough, and Los Altos Hills at the luxury tier, privacy is the dominant driver of off-market choice.

Reason 2: Price control (avoiding DOM history). On public MLS, if a listing sits 30-60 days without selling, it gets tagged "high DOM" and subsequent buyers automatically discount — "this house didn't sell, there must be a problem." Off-market carries no public DOM history, so sellers can "test the private channel for 90 days; if no qualified offer comes in, decide whether to reduce price or move to MLS," while buyers see a fresh listing without the prior private-channel history.

Reason 3: Avoiding "tested the market" stigma (withdrawal history). On public MLS, if a listing is posted and later withdrawn, Zillow and Redfin show the history — when the property re-lists later, the buyer community remembers "this didn't sell last time." Off-market carries no such public trail; if the seller decides not to sell, flow simply stops and no public record remains. This matters especially to pre-IPO founders — selling property in the window around a public listing, where a publicly recorded failure could affect reputation.

Reason 4: Test demand quietly. Sellers sometimes don't know how the market will respond and want to "test the private buyer circle first" — if qualified private offers arrive in the first week, close off-market; if not, decide whether to move to public MLS and run the standard process. This "hybrid path" is increasingly mainstream in the $10M-$15M tier — sellers don't want to forfeit the competitive-bidding upside of public MLS but want real pricing feedback from the private channel first.

Reason 5: Cross-border buyer pool concentration in off-market (especially at $15M+). In Atherton, Hillsborough, and Los Altos Hills at the $15M+ tier, a substantial share of cross-border buyers (mainland China, Singapore, Hong Kong, Taiwan) source through local brokers rather than MLS. The reason: cross-border buyers typically tour within compressed 14-30 day windows, requiring brokers to pre-prepare shortlists and run half-day curated tours — a rhythm that doesn't fit the MLS "list → public → offer deadline" flow. If your target buyer pool is cross-border HNW, off-market is the more effective channel.

The core diagnostic for whether a seller should choose off-market: (a) How high is your privacy requirement? (b) Can you accept a 3-7% trade-off in expected closing price versus a hypothetical public MLS listing? (c) Do your property attributes (tier, sub-market, distinctiveness) fit the buyer profile of the off-market pool? For Atherton $15M+ estate sellers, all three conditions typically hold — which is why off-market share runs 85-95% in that band. This section covers tax implications and ownership structures; please confirm execution details with your collaborating attorney or CPA.

How Off-Market Actually Operates in Atherton, Palo Alto, and the Luxury Tier

Off-market operates very differently across Bay Area luxury cities — the buy-side and sell-side strategies in Atherton and Palo Alto diverge sharply even when both are "luxury."

Atherton: the highest off-market share in the Bay Area. The $5M-$10M tier runs roughly 30-50% off-market (primarily Atherton Oaks, Lloyden Park, and the eastern edge of Central Atherton entry inventory); the $10M-$20M tier runs roughly 70-85% (West Atherton entry, Lindenwood, Central Atherton core); and the $20M+ tier approaches 100% (West Atherton and Lindenwood trophy estates). The drivers: the 1-acre minimum zoning, zero commercial activity town-wide, and the resident base's high privacy preference make off-market the default; combined with high cross-border buyer share and high family-office share at the $15M+ tier, where buyers almost never source through MLS. Buyer strategy: at the Atherton trophy tier, watching MLS alone effectively self-excludes; broker access to the three-layer channel architecture is mandatory. Seller strategy: Atherton $15M+ sellers who default to "just list on MLS" typically miss the best buyer pool — a compliant office exclusive is the more efficient exit path.

Palo Alto: the polar opposite. Even at $10M+, Palo Alto remains predominantly MLS-driven — 25-40% off-market, far below Atherton at the same tier. The driver: Palo Alto's PAUSD is a top-ranked U.S. school district, and family buyers in the $5M-$15M tier rely heavily on MLS (they need to search broadly across layout, attendance area, and commute); Crescent Park, Old Palo Alto, and Professorville at the high end are still dominated by school-district-driven family buyers, who source predominantly from MLS. Buyer strategy: $5M-$10M Palo Alto remains an MLS-first battleground, but $10M+ requires monitoring brokerage pre-MLS pools and TAN. Seller strategy: at the Palo Alto luxury tier, the hybrid path (private warm-up + MLS launch) outperforms pure off-market — capturing both privacy benefits and the breadth of the school-driven family buyer pool.

Hillsborough: similar to Atherton in "quiet legacy wealth" character, running 40-70% off-market. Lower Hillsborough, Upper Hillsborough, and Country Club Manor all show meaningful off-market flow, with $10M+ estate share approaching Atherton's. Buyer strategy: similar to Atherton — the three-layer channel architecture is the key. Seller strategy: office exclusive plus targeted cross-border buyer outreach is the mainstream exit at the $15M+ tier.

Woodside / Portola Valley: distinctive low-density markets. Lots typically 1-5+ acres with strong equestrian character; both sides privacy-sensitive but with slower market velocity than Atherton — closing cadence 60-180 days versus 30-90 in Atherton. Off-market share 40-60%, but on small absolute volume (Woodside closes fewer than 100 homes per year). Hyper-niche markets: the buyer pool for a Woodside equestrian estate is measured in dozens of people, and off-market broker relationships are effectively the only channel into that group.

Los Altos Hills: positioned between Atherton and Palo Alto. 35-55% off-market, with the trophy $15M+ tier rising to 60-75%. Los Altos Hills has a unique driver: town restrictions are exceptionally strict (1-2 acre minimum lot, rigorous design review, tree protection rules), and many ground-up projects begin off-market buyer sourcing during the framing phase — an off-market channel specific to Los Altos Hills.

5 Common Pitfalls in Reading Off-Market

Pitfall 1: "Assuming every broker can access the off-market pool"

Wrong. The three-layer off-market architecture (brokerage-internal / agent-to-agent / personal broker relationships) requires the broker to have real dealflow at the target city and tier — typically 5-10 years of closing experience, TAN or comparable membership, and standing in the local luxury broker peer group. The "luxury specialist" or "Compass / Sotheby's" label on a business card does not establish dealflow — direct verification is required: actual closing count at the target city and tier over the past 24 months, TAN membership status, and the ability to deliver a current off-market shortlist within 7 days of intake. The MK Group intake process in Atherton, Palo Alto, and Los Altos Hills uses this 7-day shortlist delivery as a standard diagnostic — talk-only brokers cannot deliver; brokers with real circles can.

Pitfall 2: "'Coming Soon' equals off-market"

Wrong. MLS "Coming Soon" status listings are already in the MLS database — buyers can see them on Zillow and Redfin and simply cannot submit offers immediately. This is MLS pre-launch, not off-market. After CCP 2020, true off-market must be "office exclusive" — zero public marketing, no MLS, no Zillow, with a written exclusion authorization signed by the seller. If a buyer mistakes Coming Soon for off-market, the buyer may miss the "true off-market pool" — those listings are entirely invisible on Zillow and require the broker to surface them. Sellers who think Coming Soon delivers privacy are mistaken; buyers can see the full listing details and only the offer window is delayed.

Pitfall 3: "Off-market ≠ below market (often above public MLS price)"

Wrong. Off-market closing prices typically run 3-7% lower than the hypothetical public MLS closing price for the same property (smaller buyer pool, less competitive bidding pressure), but off-market listing prices typically run higher than comparable public MLS listings — because sellers choose off-market when they hold a distinct advantage (unique lot, scarce sub-market, high-quality construction, historical reputation), and premium pricing is the norm in the off-market channel. "Off-market = bargain" is a common misconception — the true off-market pool at the Atherton $20M+ tier is in fact a premium market.

Pitfall 4: "Sellers over-relying on off-market and missing a broader buyer pool"

For $10M-$15M mid-tier sellers, pure off-market may forfeit the competitive-bidding upside of public MLS. Palo Alto $10M+ in the core sub-markets (Crescent Park, Old Palo Alto, Professorville) typically generates 3-7 offers post-MLS in active scenarios — a level of competition pure off-market cannot replicate. Diagnostic: if your property attributes (tier, sub-market, distinctiveness) fit a "broad buyer pool" — Palo Alto school-driven families, Los Altos mid-tier upgrade buyers, Menlo Park young families — public MLS or the hybrid path (private warm-up + MLS launch) outperforms pure off-market. The Atherton $15M+ estate tier is the optimal case for pure off-market.

Pitfall 5: "Buyers chasing only off-market and missing strong MLS inventory"

The mirror image of Pitfall 4. Buyers who watch only off-market and ignore MLS miss the high-quality $5M-$10M inventory that still runs predominantly on MLS — Palo Alto sub-market gems, Los Altos school-district homes, walkable Menlo Park downtown estates. The optimal strategy: use both MLS and off-market simultaneously, with the broker running two search paths in parallel from intake. At $5M-$10M, MLS weight is 60-70% and off-market 30-40%; at $10M+ the weights invert to 50-70% off-market and 30-50% MLS; at $20M+ the search is almost entirely off-market.

Frequently Asked Questions

Where can I find off-market listings in the Bay Area?

Bay Area off-market listings cannot be "searched and found on your own" — by definition off-market listings are absent from Zillow, Redfin, Realtor.com, and the MLS public database. Access to the off-market pool runs through five primary channels: (1) Select a buy-side broker with real dealflow — at least 3 actual closings at the target city and tier over the past 24 months, Top Agent Network or comparable membership-gated circle membership, and standing in the local luxury broker peer group. (2) Use the broker's brokerage-internal pre-MLS pool (Compass Private Exclusives and Sotheby's private networks are industry reference cases; other major luxury brokerages run their own internal pools). (3) Search active off-market listings via TAN and comparable agent-to-agent network platforms. (4) Activate the broker's personal local luxury broker relationships (private mailing lists, direct dial). (5) At the $15M+ tier, occasionally surface listings via wealth manager, estate attorney, or family-office introductions. At $10M+, watching MLS alone forfeits access to half or more of the inventory. Marie Wang and Kevin Mo at MK Group operate across all three layers of the channel architecture, and in the half-day curated luxury tours used for cross-border buyers a meaningful share of the homes shown are not on MLS.

What does "off-market listing" mean? Is it legal?

Off-market (also called pocket listing, private listing, or whisper listing) means the listing does not enter the MLS public database, does not appear on Zillow or Redfin, and carries no public marketing. After CCP 2020, the only compliant off-market form is "office exclusive" — zero public marketing, with the seller signing a written exclusion authorization explicitly opting out of MLS entry. Office exclusive is legal, but the listing agent must strictly observe the "zero public marketing" line — social media posts, yard signs, coming-soon stickers, etc. all trigger CCP-mandatory MLS entry. Buyers should have their broker verify that the listing agent is operating compliantly before submitting an offer; otherwise the listing may be forced back to MLS under NAR or state association review during the transaction.

What share of Bay Area listings are off-market?

By price band: roughly 5% at $1M-$3M, 15% at $3M-$5M, 25% at $5M-$10M, 50% at $10M-$20M, and 80% at $20M+ per MK Bay Area Pulse 2026 Q1 estimates. By city: Atherton 50-95% off-market (share rises with tier), Hillsborough 40-70%, Woodside 40-60%, Los Altos Hills 35-55%, Palo Alto 25-40%, Menlo Park 20-35%, Los Altos 15-30%. $10M+ is the off-market "inflection point" — once budget crosses that line, public MLS ceases to be the primary channel. Important caveat: these percentages are not MLS-published facts (by definition off-market listings are absent from the MLS database); all figures are reverse-estimates from industry observation plus known off-market closings.

Can buying off-market save money?

Not necessarily — often the opposite. Off-market closing prices typically run 3-7% lower than hypothetical public MLS closing prices for the same property (smaller buyer pool, weaker competitive pressure), but off-market listing prices typically run higher than comparable MLS listings — because sellers choose off-market when they hold distinct advantages (unique lot, scarce sub-market, high-quality construction, historical reputation), and premium pricing is the norm in the off-market channel. "Off-market = bargain" is a common misconception. Off-market listings in the Atherton $20M+ band frequently price 5-15% above comparable MLS listings — the premium reflects scarcity rather than broker markup. The real value of off-market is "seeing most of the inventory you would otherwise never see", not "saving money."

When should a seller choose off-market?

Five real drivers: (1) Privacy — well-known families, public-company executives, cross-border entrepreneurs, AI / tech founders who don't want Zillow showing neighbors. (2) Price control — avoiding public DOM history that triggers automatic discounting from subsequent buyers. (3) Avoiding withdrawal history — if the decision is not to sell, off-market leaves no public trace. (4) Test demand quietly — 90-day private warm-up; move to MLS only if no qualified offer arrives. (5) Cross-border buyer pool concentration off-market (especially at $15M+). Trade-off: off-market closing typically prices 3-7% below hypothetical MLS, but for privacy-sensitive sellers or $15M+ tier sellers, the trade-off is acceptable. The diagnostic: your privacy requirement, whether your property attributes fit the off-market buyer profile, and the closing-price trade-off you can accept. Atherton $15M+ estate sellers typically meet all three — which is why off-market share runs 85-95% at that tier.

Next Steps

- Confirm your tier and role — is it $5M-$10M, $10M-$20M, or $20M+? Buy side or sell side? The off-market strategy diverges sharply by tier and role: $5M-$10M remains an MLS-first battleground; $10M+ enters off-market-dominant territory.

- Verify your broker has real dealflow — actual closing count at the target city and tier over the past 24 months, TAN or comparable membership-gated circle membership, and ability to deliver a "current off-market shortlist matching your profile" within 7 days of intake. This is the hard test of real dealflow.

- Buy side: open both MLS and off-market channels in parallel — $5M-$10M weights MLS 60-70% and off-market 30-40%; $10M-$20M inverts; $20M+ runs almost entirely off-market. Don't use a single channel.

- Sell side: evaluate the three paths (on-market / off-market / hybrid) — based on privacy requirements, property attributes, tier, and timing flexibility. $5M-$10M still rewards public MLS competitive bidding; $10M-$15M mainstream is hybrid (private warm-up + MLS launch); $15M+ pure off-market is the optimal estate-seller path.

- Sell side: verify your listing agent's CCP understanding — office exclusive requires strict zero public marketing; any social media, yard sign, or coming-soon sticker triggers mandatory MLS entry. Ask the listing agent for a written exclusion authorization template plus a detailed walk-through of what counts as public marketing.

- Cross-border buyers: prepare a 14-30 day compressed tour window plus a half-day luxury tour cadence — at the $15M+ tier, cross-border buyers rarely source via MLS; flow runs through the broker's pre-prepared off-market shortlist plus half-day curated tours. This cadence diverges fundamentally from the MLS "list → public → offer deadline" flow and requires the broker to align on profile 30-60 days ahead.

- All sides: understand the uncertainty in the share figures — all off-market share numbers are reverse-estimates from industry observation plus known closings (by definition off-market listings are absent from the MLS database); actual share may vary 5-10 percentage points. Treat them as "tier-structure" reference, not absolute numbers.

Further Reading

- 🏛️ Buying in Atherton: Complete $10M+ Luxury Buyer's Guide — Buy-side strategy and 6-step process for the Atherton off-market-dominant market

- 🏘️ Selling in Atherton: Complete $10M+ Luxury Seller's Guide — On-market vs off-market vs hybrid path selection for Atherton sellers

- 🏡 Buying in Palo Alto: 7 Sub-Markets Complete Guide — Palo Alto luxury as the MLS-dominant contrast reference

- 🏙️ Selling in Palo Alto: Complete Seller's Guide — PA tier MLS competitive-bidding upside and hybrid path selection

- 🏗️ Atherton / Hillsborough / Woodside $10M+ Luxury Builders — Ground-up builder direct as a key off-market channel at the Atherton $15M+ tier

- 🌏 Cross-Border Buyer Complete Guide for the Bay Area — $15M+ cross-border half-day curated luxury tour + off-market shortlist process

- 📁 Where Silicon Valley's Elite Circles Actually Meet — The mechanism by which Atherton off-market listings circulate inside the inner circle

- 📁 Shenzhen entrepreneur closes a $9M+ Los Altos home in a single-day cross-border luxury tour — Real cross-border buyer case using an off-market shortlist plus half-day curated tour