Direct Answer

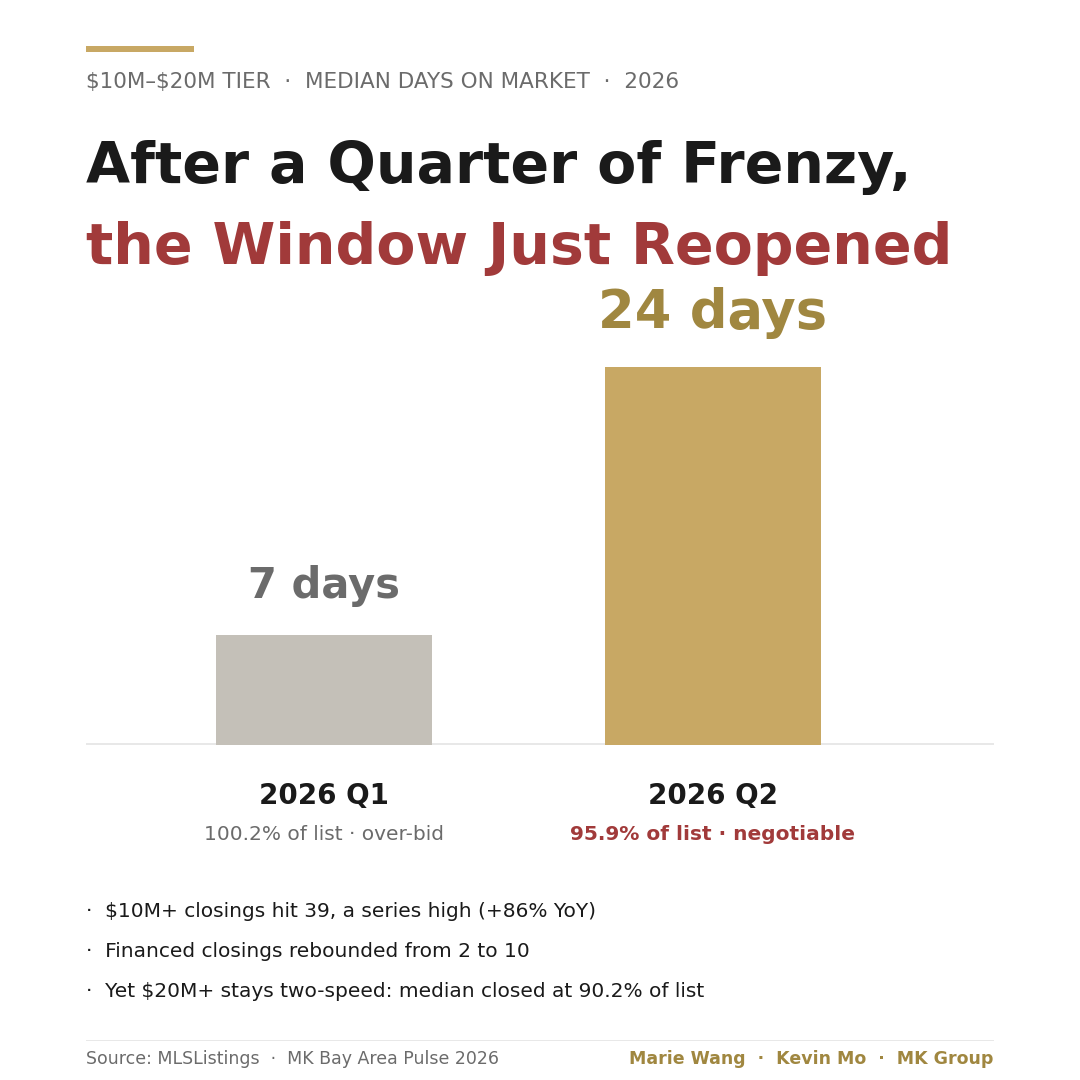

Yes — and far more easily than a quarter ago. In Q1 2026 the $10M+ market was a scramble: the $10M–$20M tier closed in a median of seven days at 100.2% of original list, bid over asking. By Q2 the same tier had cooled to a 24-day median and a 95.9% median close (below asking), $10M+ supply climbed to a series-high 39 closings, and financed deals rebounded from two to ten. The negotiating window reopened after a quarter of frenzy — but not every $10M+ home is negotiable; the pricing start still decides.

This article is for decision-making education and does not constitute investment, bidding, or financing advice; confirm the specifics with your agent, attorney, and lender.

Who This Article Is For

- Buyers with $10M+ shopping Atherton, Palo Alto, Los Altos Hills, or Woodside, trying to read whether now is the time to move and whether there is room to negotiate.

- Buyers who stepped back in late-2025 because they kept getting out-bid, wanting to know if Q2 has left a window open.

- Sellers preparing to list a $10M+ home and weighing how high to set original list — and how that starting number will govern both speed and final price.

- Cross-border and pre-IPO buyers sizing a cash-versus-leverage mix at this tier for the first time, who want to understand what the return of financing means.

One: Three Signals the Window Reopened — Days on Market, Sale-to-List, Supply

"The window reopened" is not a feeling; it is three measurable signals turning together between Q1 and Q2. The headline first: in the $10M–$20M tier, median days on market stretched from Q1's 7 to Q2's 24, the median close slid from 100.2% of original list to 95.9%, and $10M+ quarterly closings hit a series-high 39.

Signal 1: Days on market went from 7 to 24 — buyers got time back

A 7-day median meant a $10M+ home had to be decided within a week, with almost no room for inspections or negotiation — you won on speed and price alone. Q2's 24 days more than tripled that runway: at the median you now have time to do diligence, to compare, to negotiate in rounds. Time itself is the most basic form of leverage — a buyer forced to decide overnight has none; a buyer who can wait a week has some.

Signal 2: Sale-to-list fell from 100.2% to 95.9% — the over-asking premium vanished

Q1's 100.2% was a seller's-market reading: the median close cleared original list, and the fastest, highest bid won. Q2's 95.9% flipped that — the median close landed about four points below original list. This is not a crash; it is the return from "bid over" to "negotiate under list." On a $12M home, four points is close to $500K — and that is only the median. Deal by deal, as the table below shows, the dispersion is far wider.

Signal 3: Supply hit a series-high 39, financed deals back from 2 to 10 — choice and leverage returned together

Q2 saw 39 $10M+ closings across the Bay Area, a high for our quarterly series (+86% versus 21 in Q2 2025). More supply means more lateral choice — the confidence that "if this one falls through, there's another" is exactly what shifts leverage from seller to buyer. At the same time, financed $10M+ deals rose from 2 in Q1 to 10 in Q2: the "all-cash or out" squeeze eased and leveraged buyers re-entered, restoring depth. Why leverage returned — the stock-market and rate math behind it — is unpacked in the Q2 return of luxury leverage.

Two: Not Every Home Is Negotiable — the Two-Speed Market Above $20M

The reopening is a tier-level median. On individual homes it is highly dispersed, and $20M+ shows it best: a two-speed market where market-priced homes still get grabbed — even over asking — while over-anchored ones drift down to a discount. The difference is not how grand the home is; it is whether original list was set near the market.

The core numbers: in Q2 2026 the Bay Area recorded six $20M+ public closings, a 44-day median at 90.2% of original list (a roughly 9.8% median discount). But laid out one by one, they run from 80.4% (well below asking) all the way to +17.8% over asking.

| Home (Q2 2026 · $20M+ closing) | Original list | Sold | Sale/list | DOM | Payment |

|---|---|---|---|---|---|

| Atherton · 77 Flood Cir | $34.5M | $27.75M | 80.4% | 70 | Cash |

| Palo Alto · 444 Tennyson | $24.89M | $22.0M | 88.4% | 97 | Financed |

| Atherton · 167 Almendral | $24.5M | $21.9M | 89.4% | 98 | Cash |

| Atherton · 241 Polhemus | $25.0M | $22.75M | 91.0% | 8 | Cash |

| Atherton · 98 Flood Cir | $20.0M | $22.0M | 110.0% | 18 | Cash |

| Atherton · 60 Ralston | $18.0M | $21.2M | 117.8% | 4 | Cash |

The pattern to hold onto: this table is essentially sorted by whether original list was set right. The two over-asking closings (98 Flood Cir at $20M, 60 Ralston at $18M) had the most restrained starting prices — priced to the market, they drew competition and cleared over list in 4 to 18 days. The two deepest discounts (77 Flood Cir at $34.5M closing 80.4%, 444 Tennyson at $24.89M closing 88.4%) carried the highest original asks — anchored high, they sat 70 to 98 days and found the market only after a 9%–20% discount. So "is $20M+ negotiable" is the wrong question; what matters is how far a home's original price sits from the market, not which tier it is in. That the list price at the top is often just the seller's aspiration — negotiable year-round — is a separate, evergreen mechanism, unpacked in do $20M+ homes really sell below asking. This piece is about timing: what changed in one tier between Q1 and Q2.

Three: The Buyer's Playbook — Two Different Offers for "30+ Days" vs "Freshly Listed"

A reopened window does not mean the same slow-negotiation playbook works on every home. The tier's 95.9% is a highly dispersed median — half the homes sat past 24 days, half moved faster. Read which half a home is in before you set your posture.

On over-anchored homes sitting 30+ days: this is where the room is

When a $10M+ home's current days on market clearly exceed the tier median (24) and its original list was set high, the seller's anchor is being tested — this is where you open below asking and negotiate in rounds. Pull the full listing history first: original list, any price cuts, how many, how long on market. The higher the anchor and the longer the sit, the firmer your footing. In the table above, 77 Flood Cir — 70 days, closing at 80.4% — is the extreme of this type.

On freshly listed, market-priced homes: speed is still your friend

Run the other way: a home just listed at a restrained, market price will most likely still move fast — "the window reopened" does not help you here. 60 Ralston listed at $18M and closed in 4 days at +17.8%; 98 Flood Cir listed at $20M and closed in 18 days at +10.0%. Carrying a blanket "the market softened, I can take my time" onto a sharply priced new listing is the easiest mistake to make in this window.

Cash vs leverage: a financed offer is no longer the Q1 liability

A structural Q2 shift is the return of leverage — $10M+ financed closings went from 2 to 10. The mechanism: the market rose about 20.9% over the past year, so selling stock to raise all cash means exiting a still-compounding position and taking an immediate capital-gains hit, while mortgage or securities-based credit near 6.4% often costs less than these buyers' expected portfolio return. Using leverage here is opportunistic, not a dependency — a financed offer no longer washes out the way it did in Q1's scramble. But do not read that as "terms can loosen": in bilateral negotiation, clean, high-certainty terms (all cash, or pre-approved with a fast close) remain leverage. The full cash-and-pre-IPO funding path is in turning pre-IPO stock into a Bay Area luxury home.

Four: How Long Will the Window Stay Open? Honestly — One Quarter Can't Say

This has to be said plainly, so it is not misread as "the turn is in, sit and wait." Q2's 24 days / 95.9% is one window after a quarter of frenzy — it could be a single-quarter breather or the start of a sustained shift, and one quarter of data cannot tell you which. The macro backdrop is mixed: the 30-year mortgage at 6.41% (down 37bps year over year, but up 31bps quarter over quarter), the S&P at record highs (+20.9% YoY) still minting buyers, and the Case-Shiller San Francisco index turning positive year over year (+2.47%). These forces pull against each other; there is no one settled direction. Whether to move in this window turns on your own timeline and the scarcity of the home, not on a bet that next quarter softens further. Whether the window widens or narrows is for the next MK Bay Area Pulse to confirm — do not treat a single quarter as a trend.

Local Data: $10M–$20M and $20M+ Across Three Quarters

The headline first: the $10M–$20M tier's negotiating strength traces a clear arc — a 7-day median at 100.2% of original list in Q1 2026, back to 24 days at 95.9% (below asking) in Q2. The $20M+ tier stayed "slow and negotiable" across all three: 80 days / 82.4% in Q2 2025, briefly tightening to 9 days / ~100% in Q1 2026, then back to 44 days / 90.2% in Q2.

| Tier | Quarter | Closings | Median DOM | Median sale/original |

|---|---|---|---|---|

| $10M–$20M | 2025 Q2 | 18* | —** | —** |

| $10M–$20M | 2026 Q1 | 15 | 7 | 100.2% |

| $10M–$20M | 2026 Q2 | 33 | 24 | 95.9% |

| $20M+ | 2025 Q2 | 3 | 80 | 82.4% |

| $20M+ | 2026 Q1 | 6 | 9 | ~100% |

| $20M+ | 2026 Q2 | 6 | 44 | 90.2% |

* Combined $10M+ was 21 closings in Q2 2025 (of which 3 were $20M+) and 39 in Q2 2026 — up 86% and a series high. ** Small sample that quarter; median DOM and sale-to-list not broken out for this sub-tier.

What to hold onto: the words "window reopened" are carried by the $10M–$20M Q1-to-Q2 columns — 7 to 24 days, 100.2% to 95.9%. The $20M+ tier is the caution against over-reading it: it tightened briefly in Q1 (9 days) and loosened again in Q2 (44 days) — a small, volatile sample whose median must be read alongside the deal-by-deal table above, or its six-closing median will mislead.

Data sources: MLSListings public closing records / MK Bay Area Pulse 2026 Q2 / H1 2026

Last updated: 2026-07

Scope: Bay Area (Peninsula / South Bay; Santa Clara / San Mateo / Alameda counties) single-family closings above $10M; the $10M–$20M and $20M+ tiers are small samples, flagged deal by deal.

The MK Group Field Observation: What Negotiating in a Window Looks Like

Data tells you the window reopened; whether you turn it into an advantage depends on whether you dare to negotiate and can read the seller's situation. MK Group's two founders, Marie Wang (DRE# 02110980) and Kevin Mo (DRE# 02127623), happened to handle — in that negotiable late-2025 window — a deal that shows exactly what negotiating in a window looks like.

In late 2025, a family working at a leading AI company came to MK Group: they had liquidated pre-IPO company stock in tranches on the secondary market and were buying a Los Altos Hills estate all-cash, the goal being to lock a home before the company's IPO sent a wave of newly wealthy colleagues sweeping the top of the market. Many would assume that an all-cash buyer under time pressure to close before an IPO is a "whatever the seller asks" buyer. Instead, once MK took over the negotiation, drawing on a long read of luxury supply and demand and a feel for the seller's psychological timing, they brought the price down by more than $1M from original. That is what negotiating in a window looks like: even as a cash buyer, even under a clock, when the market sits in a negotiable window and you read the seller's motivation, a $1M+ of room is real and reachable.

Placed back on this article's timeline, that deal carries a second lesson: the late-2025 window was squeezed shut by Q1 2026's scramble (the $10M–$20M tier briefly at 7 days and 100.2%), and only reopened in Q2. Windows open and close — the same Los Altos Hills home can offer wildly different room depending on whether you move in a window or a frenzy. So the question more useful than "are luxury homes negotiable" is: which market am I standing in right now? Read days on market, original pricing, and supply depth together, and you will know whether to enter with speed or with patience.

(The case above is anonymized: the client is described only as "a family working at a leading AI company," with no name, title, share count, or absolute closing price; the $1M+ of negotiating room comes from a real transaction in MK Group's own record. Tier-level closing figures are from MLSListings public closings / MK Bay Area Pulse 2026 Q2.)

Common Mistakes

Mistake 1: "After a Q1 like that, $10M+ still means bidding over to win"

No. Q1 was indeed an extreme scramble — the $10M–$20M tier closed in a median of 7 days at 100.2% of original list. But by Q2 the same tier was back to a 24-day median and a 95.9% close (below asking), with supply at a series-high 39. Carry Q1's urgency intact into Q2 and the direct result is overpaying in a market that can now be negotiated (source: MK Bay Area Pulse 2026 Q2).

Mistake 2: "A reopened window means every $10M+ home is negotiable"

Wrong. The reopening is a tier median; deal by deal it is highly dispersed. $20M+ is the classic two-speed market: 60 Ralston listed at $18M and closed in 4 days at +17.8%, while 77 Flood Cir listed at $34.5M closed 70 days later at just 80.4%. Whether a home is negotiable turns on how far its original list sits from the market, not which tier it is in. Bring a "the market softened" mindset to a sharply priced new listing and you will neither move it nor win it (source: MLSListings Q2 2026 closings).

Mistake 3: "30+ days on market means something's wrong — negotiate freely"

Read it with the original price; do not treat days on market alone as a discount guarantee. Long sits come in two kinds: original list set high and the anchor slowly disproven by the market (real room here), or a seller in no hurry, content to wait for the right buyer (you will not move them). The 70-to-98-day homes in the $20M+ table are mostly the former, but sellers who sit for months and give nothing exist too. Treating DOM as sufficient grounds to negotiate is an easy misread (source: MK Bay Area Pulse 2026 Q2).

Mistake 4: "$10M+ requires all cash — a financed offer is out"

That was Q1's scramble; it no longer holds in Q2. $10M+ financed closings rose from 2 to 10 — the return of leverage means a financed offer is no longer an automatic liability. The reason: with the market up 20.9% over a year, raising all cash means exiting a compounding position and taking a capital-gains hit, while credit near 6.4% often costs less than expected portfolio returns, making leverage an opportunistic choice. But do not read it as "terms can loosen": in bilateral negotiation, clean, high-certainty terms (all cash, or pre-approved with a fast close) are still leverage (source: MK Bay Area Pulse 2026 Q2).

Next Steps

- Pull "original list → current list → days on market" as a set — a high original price plus 30+ days on market is the real signal of room, not a blanket "luxury is always negotiable."

- Keep your speed on freshly listed, market-priced homes — in Q2 restrained pricing still cleared over asking in 4–18 days; do not misread "the window reopened" as "everything can be negotiated slowly."

- Settle your funding structure early — Q2's return of leverage means a financed offer is no longer out, but clean, certain terms remain leverage at the table. The cross-border cash and pre-IPO path is in turning pre-IPO stock into a Bay Area luxury home.

- Do not treat one quarter as a trend — Q2's 24 days / 95.9% is one window after a frenzy; whether it widens or closes is for the next MK Bay Area Pulse to confirm. Cross-check the Bay Area off-market channel guide to gauge how many closings never touch public MLS.

- First decide whether you are in a "window" or a "frenzy," then choose speed or patience — the top-tier mechanism of "list price as aspiration, negotiable year-round" is in do $20M+ homes sell below asking.

⚠️ This article is for decision-making education and does not constitute investment, bidding, tax, or financing advice; confirm the transaction structure and funding arrangements with your agent, attorney, CPA, and lender.