Direct answer

No one can time a financial crisis — whether it comes, or when. The lesson worth taking isn't the prediction; it's the defensive structure the wealthy are quietly building: more cash, assets that pay rent and interest rather than chase price, less leverage, and more holdings outside the public markets. What any household can borrow is that logic itself — not a decision to sell everything and wait for a crash.

Who this article is for

- Families with real assets who worry about macro risk but don't want to sell blindly into fear

- Readers who want to see exactly how the genuinely wealthy defend under a crisis warning

- Buyers weighing a Silicon Valley purchase who want to understand the role a luxury home plays inside a full portfolio

- Anyone tracking the Fed, US debt, AI valuations, and commercial real estate who wants to translate those signals onto their own balance sheet

- Long-horizon investors who prefer to meet uncertainty with structure, not with market-timing

Three decision dimensions

Faced with a warning like "the biggest financial crisis could arrive within 18 months," most people default to one of two moves — ignore it entirely, or sell everything in a panic. Both are wrong. The wealthy sit between the two: they don't bet on the timing, they adjust the shape of their assets so they're comfortable whether the crisis comes or not. To decide your own path, think through three dimensions first.

Dimension one: are these risks stacking at the same time, or isolated events?

A single risk signal isn't frightening. What's frightening is when the same environment ties several of them together. Right now, US debt, AI valuations, and commercial real estate all trace back to one fuse — high interest rates. When rates are high, the government's debt costs more, growth-stock valuations are harder to justify, and office loans are harder to refinance. So the first question isn't "which signal is scariest," it's "are they reinforcing each other?" Three lights flashing red at once means something very different from one climbing in isolation.

Dimension two: does your wealth live on price appreciation, or on cash flow?

This is the core of how the wealthy reshape a portfolio. Assets that live on appreciation — growth stocks bought for the spread, holdings priced purely on future upside — bleed first when the market turns. Assets that live on cash flow — rental property, private credit, infrastructure that pays steady distributions — hold up better, because tenants still pay rent each month and borrowers still service their debt. Working out the ratio between these two in your own portfolio is more useful than guessing the date of a crash.

Dimension three: if the crisis actually comes, can you act?

A crisis is a disaster for the unprepared and an opportunity for the prepared. Two things decide which side you land on: cash and leverage. Someone holding cash with low leverage can buy at a discount while others sell in panic. Someone fully invested and levered up can be forced to liquidate the moment the market turns. So the third dimension is a question to yourself: if assets fell 20% across the board tomorrow, would you be taking the hit passively, or would you have room to act?

The three risk signals, at a glance

The headline numbers first. US federal debt has reached $38.5 trillion — about 127% of GDP, against an internationally recognized safety line of 60%. This year, for the first time in history, the government's interest expense exceeded the military budget: of every $3 in tax revenue, close to $1 now goes straight to interest. The S&P 500's Shiller CAPE ratio sits at 39x, a level only the 1999 dot-com peak has ever exceeded. And the national office vacancy rate is 20.7%, an all-time high — roughly one in five offices standing empty.

| Risk signal | Key number | Reference / meaning | Source |

|---|---|---|---|

| Sovereign debt | US debt $38.5T ≈ 127% of GDP | Safety line 60%; interest expense topped the military budget for the first time this year | US Treasury / IMF |

| AI valuations | S&P 500 Shiller CAPE 39x | Only 1999 ran higher; Big Tech AI spend ~$560B vs ~$35B in AI revenue (~16x) | Public market data / company filings |

| Commercial real estate | Office vacancy 20.7% (all-time high) | One in five empty; ~$930B in CRE loans mature in 2026, ~3x the historical average | Morningstar DBRS |

What matters most: these three aren't isolated. They're strung together by the same high-rate environment, stacking at once. On debt, the IMF projects that if policy doesn't change, the US debt-to-GDP ratio climbs to 140% by 2031 — a point at which the government has almost no fiscal room left. On commercial real estate, the office-mortgage default rate has jumped from under 2% a few years ago to 12.3% in January 2026 — roughly one loan in eight now in default — and Morningstar DBRS expects more than half of the CRE loans maturing in 2026 to miss timely repayment. One clarification on AI: the problem isn't whether the technology works. It's that the arithmetic — spending 16 times what the business earns — doesn't add up yet. Multiple institutions project this capital spending will keep climbing sharply, and if reality can't keep pace with the "perfect future" the market has priced in, there is a great deal of room to correct.

What MK Group sees in the field

In the Silicon Valley market, the same logic gets more concrete. In this video, Kevin Mo shares two observations from the ground worth unpacking on their own.

The first is speed to sale. Take Atherton — one of the most expensive luxury enclaves on the Peninsula. A year ago, the average time from listing to sale ran about 150 days, or five months. This year it's down to roughly 48 days, about six weeks — close to three times faster. But Kevin Mo is careful to add a caveat: Atherton closes only a few dozen sales a year, and one or two headline estates can skew that average, so the figure reads better as a directional signal than a precise metric. What it tells you is that even amid the crisis warnings, liquidity at the top of the market remains strong.

The second, and more important, is holding structure. Kevin Mo notes that a growing share of high-end buyers here don't purchase in their own name at all — they hold through a trust or an entity. The logic reduces to one line: separate ownership of the home from the individual. Once a home goes into an irrevocable trust, it's legally no longer your asset — title passes to a trustee, the benefit stays with your family, and you deliberately give up control. With that step done, if a lawsuit or debt dispute later lands on you personally, a creditor generally can't reach the house. You might ask: doesn't putting cash into a trust do the same thing? In principle, yes — but cash has an unavoidable problem. People can't bring themselves to truly let go of it, and the moment you can withdraw at will, the separation is legally hollow. A house is different: you didn't need to touch it daily anyway, so surrendering control barely affects your life, and in exchange you gain a real legal firewall. That's why, in the wealthy family's risk-isolation toolkit, a luxury home is often more useful than cash (trust structures involve legal and tax questions — confirm the specifics with your attorney and CPA before acting).

Behind this is a view of risk that differs from most people's: these buyers aren't scrambling to fix things once the crisis arrives — they've already thought through "what if something goes wrong" at the moment of purchase. It's a pattern Marie Wang (DRE# 02110980) and Kevin Mo (DRE# 02127623) see repeatedly with the families they serve in Atherton and Palo Alto. For those owners, a luxury home isn't playing the role of a speculative trade on price — it's playing the role of something that carries you through the cycle, and that durability is itself part of what makes Peninsula property worth holding.

Common misconceptions

"The crisis calls are this loud — I should sell everything and wait for the crash"

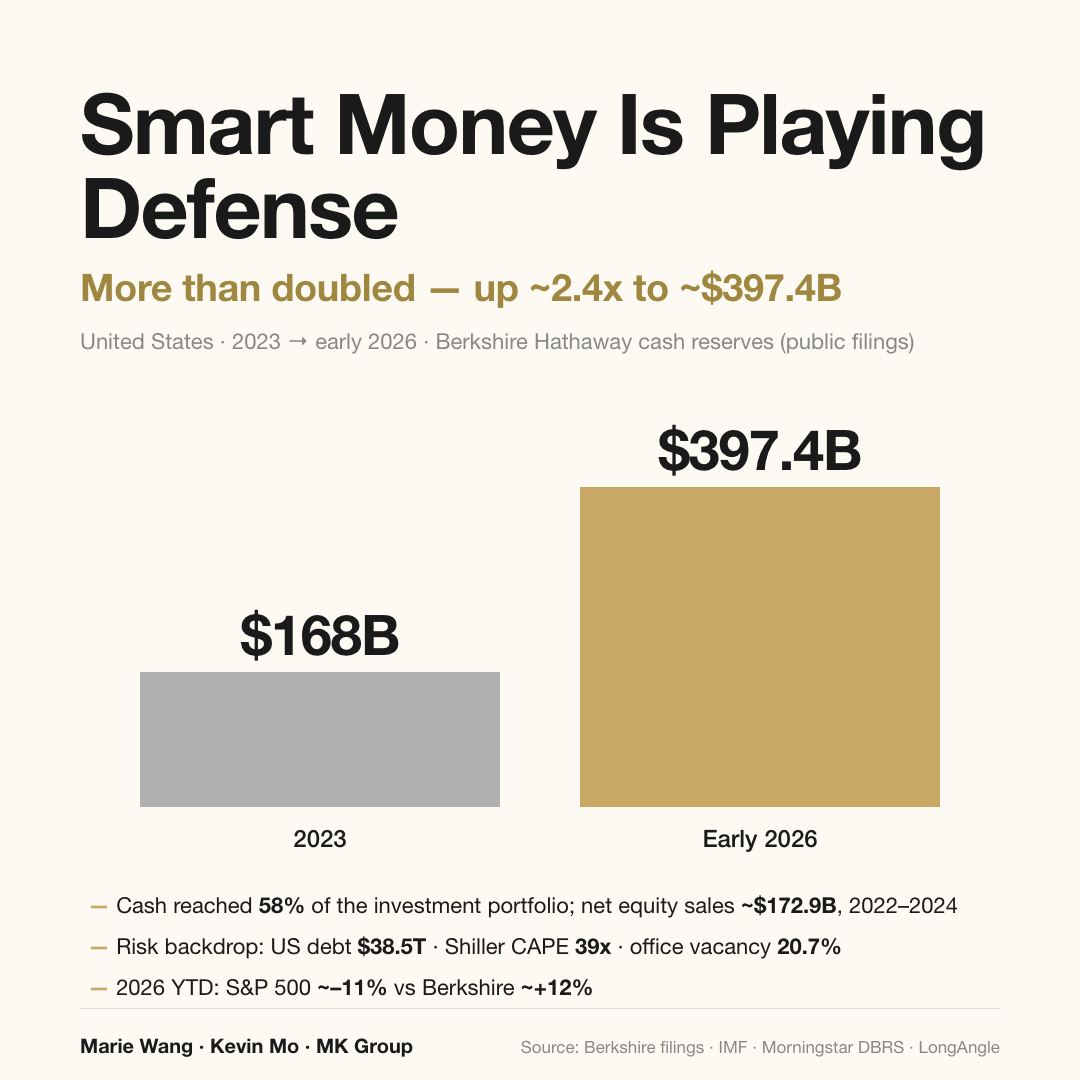

No one can predict with certainty whether a crisis comes, or when — even someone who has warned publicly three times can't hand you a detonation date. Selling everything to wait for a crash risks missing on both ends: if the crash keeps not coming, you miss the gains in the meantime; if it does come, you may not catch the bottom anyway. Watch what the wealthy actually do. Berkshire Hathaway was a net seller of about $172.9B in equities across 2022–2024 (roughly $134.1B in 2024 alone) — but that wasn't a panicked, one-shot liquidation. It was quiet, steady trimming, while the cash pile climbed to about $397.4B by early 2026. Nor is Buffett an outlier: LongAngle's 2026 survey of more than 200 high-net-worth investors (average net worth $17M) found its conservative cohort holding as much as 27% in cash, and Goldman Sachs data shows affluent investors averaged roughly 20% in cash and short-duration bonds in 2024. Defense is reshaping the structure, not pulling the plug.

"Putting cash in a trust and putting a house in a trust do the same thing"

They don't — and the difference is exactly whether you can truly let go. Asset isolation through a trust depends on surrendering control. Put cash in a trust but keep the ability to withdraw at any time, and that isolation is legally close to hollow. A house is the opposite: you didn't need to touch it daily, so giving up control barely changes your life, and in return you gain a solid legal firewall. That's why a luxury home is often more useful than cash for risk isolation. (This is legal and tax structuring — the direction is worth understanding, but how you execute should follow the guidance of your own attorney and CPA.)

"In a crisis, Peninsula luxury homes will fall just like stocks"

Let's be honest: any asset can come under pressure in a systemic crisis. A luxury home won't "never fall," and treating it as a can't-lose safe haven is its own mistake. But the role it plays in a wealthy portfolio was never to chase a short-term spread — it's a reliable hold: liquid, able to carry legal isolation, and holding long-term use and value. The test of whether it's worth owning is "can it get through a cycle," not "will it dip next quarter."

Next steps

- Watch the Fed's cadence. Today's high rates are the shared root of all three pressures — debt, AI valuations, commercial real estate. When large rate cuts begin, it usually means one of two things: inflation is genuinely contained, or the economy has hit real trouble that needs rescuing. Both are turning points for every asset class.

- Track whether executives are selling their own stock in size. You can check the public disclosures directly on SEC EDGAR; if a company's CEO or CFO starts steadily unloading large amounts of their own shares, that's a signal worth heightened attention.

- Re-examine your own debt structure — the most practical move, and the one most within your control. If your debt ratio runs high, seriously consider cutting consumer borrowing and setting aside a few months of living reserves, and don't chase assets that depend heavily on a hot economy just because the market is hot.

- Check your cash and leverage positions, so that if the crisis does come you have the capacity to act — rather than getting crushed by leverage when the market turns.

- If you're weighing a Silicon Valley purchase, first get clear on the role the property plays in your overall structure — a long-term hold with legal isolation, or a short-term bet on price — then decide how to hold it (individual name / trust / entity), and consult your attorney and CPA on the structuring details.