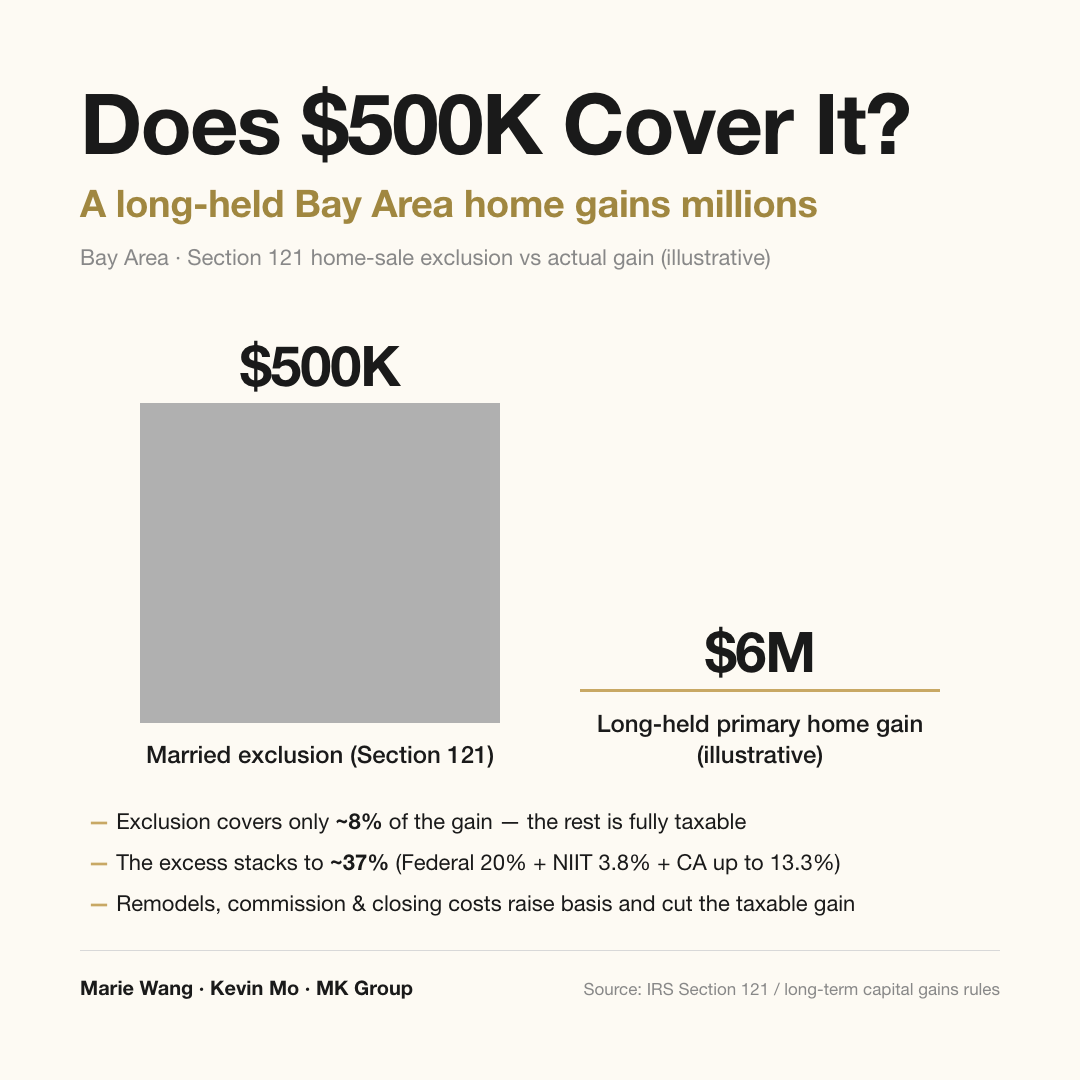

The Direct Answer

Section 121's $250K (single) / $500K (married) exclusion applies to the gain on your home, not the sale price—and a long-held Bay Area home's gain runs into the millions, so the exclusion usually covers only a sliver. The rest is taxed as long-term capital gain: federal up to 20% + NIIT 3.8% + California taxing capital gains as ordinary income (up to 13.3%), stacking to roughly 37% at the top-end margin. Paying less comes from building your cost basis fully and deducting every selling cost—not from counting on that half-million.

Who This Article Is For

This is written for one very specific reader: you have held a primary home in the Bay Area for a long stretch—maybe bought fifteen or twenty years ago, maybe pushed up in the recent tech-wealth wave—and you are now seriously considering a sale, with one question at the front of your mind: how much of the proceeds actually stays with me? You have probably heard that "a primary home gets a $500K exclusion," and you sense that with your home's appreciation $500K clearly will not be enough—but you cannot pin down exactly how the excess is figured, who it goes to, or whether any of it can be trimmed. If you own jointly as a married couple, or the home was briefly rented out, or it came to you through inheritance or a divorce, this also flags the edge rule that applies to you. It is about the take-home math at the point of sale—not deferral on an investment property, and not the holding structure you set up before buying. This is also the question Marie Wang (DRE# 02110980) and Kevin Mo (DRE# 02127623) field most often from high-appreciation Bay Area sellers.

Three Core Judgment Dimensions

Behind "is the $500K exclusion enough" sit three separate accounts you have to run apart. Read these three clearly first, and only then does "how much stays with me" come out right.

First, the exclusion reduces the gain, not the price—and it has a threshold. Section 121 lets you exclude $250K (single filer) / $500K (married filing jointly) from your capital gain—and the gain here is "sale price minus cost basis," not the total closing figure. So whether a home that closes at $4.5M gets any use out of the exclusion, and how much tax is left after it, turns on how large your true appreciation is, not on the headline sale number. Do not skip the threshold either: within the five years before the sale, the home must have been your primary residence for at least 2 years (24 months, and they need not be consecutive) and owned for at least 2 years; for a married couple to claim the full $500K, both spouses have to meet the use test; and you can only use this exclusion once every two years. Miss the threshold and the $250K/$500K drops to zero.

Second, the part above the exclusion is taxed in three stacked layers. This is where "$500K is nowhere near enough" bites hardest. The excess is taxed as long-term capital gain (held over a year), and for a high-income California seller the real-world exposure is a stacked rate: federal long-term capital gains of 0% / 15% / 20% (large gains land at 20%) + the Net Investment Income Tax (NIIT) of 3.8% (on the portion of MAGI above $250K married / $200K single) + California taxing capital gains as ordinary income (up to 13.3%). Stack the three and the top-end marginal rate on a large gain runs about 37%. In plain terms, on every $1M of gain above the exclusion, roughly $370K at the top goes to tax.

Third, cost basis and selling costs are the only legal levers to push the taxable gain down. Taxable gain = (sale price − selling costs) − (purchase price + capital improvements) − exclusion. Two terms in that formula are ones you can actively enlarge: one is cost basis—the capital improvements you made over the years (additions, kitchen/bath rebuilds, roof or HVAC replacement, permanent hardscape) all add to the purchase price when you have the contracts, invoices, and permits; the other is selling costs—agent commission (roughly 5%), transfer tax, and escrow/title fees, all subtracted off the top of the sale proceeds. Draw the line carefully: what raises basis is a capital improvement, while routine maintenance and pre-sale touch-up painting generally count as repairs and do not. Build these two out fully and you can shave the taxable gain by hundreds of thousands—sometimes more than a million.

How the Three Layers of Tax Stack on the Excess: Start With These Numbers

The core figure first: the slice of gain above the Section 121 exclusion, in a high-income California seller's hands, carries a top-end marginal rate of about 37.1% = federal 20% + NIIT 3.8% + California up to 13.3%. Put another way, for every additional $1M of taxable gain beyond the $500K exclusion, roughly $370K at the top goes to tax. The table below breaks that stack apart:

| Tax | Rate | Trigger / Note |

|---|---|---|

| Federal long-term capital gains | 0% / 15% / 20% | Held over one year; large gains for high earners land at 20% |

| NIIT (Net Investment Income Tax) | 3.8% | On the portion of MAGI above $250K (married) / $200K (single) |

| California state tax | up to 13.3% | Capital gains taxed as ordinary income; 13.3% on income over $1M |

| Top-end combined | approx. 37.1% | Marginal stack on large gains (not all gain reaches the top) |

The thing to hold onto: this 37% is the top-end margin, not a flat rate on the whole gain—the stack is tiered, the lower brackets are lighter, and only the slice that pushes you into the top band pays the full 37%. But a long-held Bay Area home's gain, routinely in the millions, often shoves most of itself straight into the federal 20% and California 13.3% top bands in one motion—so for a high-appreciation seller, estimating the tax on the portion above the exclusion at "close to 37%" is usually right within a hair.

Here is one order-of-magnitude illustration (a general projection, not any real transaction): a married couple buys a Palo Alto single-family home in 2004 for $1.4M, does $300K of documented kitchen/bath rebuild and addition over twenty years (added to basis), and sells in 2026 for $4.6M, with commission + transfer tax + escrow of about $270K. Their taxable gain = ($4.6M − $270K) − ($1.4M + $300K) − $500K exclusion ≈ $2.13M. At a top-end estimate of about 37%, the tax runs roughly $780K. Had they kept no remodel records and folded in no selling costs, the same home's taxable gain would be computed at about $2.7M—roughly $200K more tax—the entire difference riding on whether basis and selling costs were built out.

Data sources: Section 121's $250K/$500K exclusion, the 2-of-5-year use and ownership test, and the once-every-two-years limit come from official public IRS rules; the 0%/15%/20% long-term capital-gains brackets and the 3.8% NIIT come from the IRS; California taxing capital gains as ordinary income at a top marginal rate of 13.3% comes from the California FTB. The purchase price, sale price, remodel, and commission in the illustration are general projections used to show how the tax is built up—not real transaction data.

Last updated: 2026-07

Scope: California tax residents selling a long-held primary residence in the Bay Area. Rates and thresholds follow the IRS / FTB rules in force in the year of sale.

The MK Group Field Observation: The Real Account Isn't "How Much It Rose"—It's "How Much of the Gain Is Taxable"

With high-appreciation Bay Area sellers, MK Group (Marie Wang and Kevin Mo) keeps seeing the same gap: everyone fixes on "this home went up a few million" and feels great about it, yet almost no one, before selling, works out "of those few million, how much turns into taxable gain"—and the two numbers are often far apart.

Look first at how far the exclusion falls short. A high-net-worth family we assisted had years earlier bought a 7,000-square-foot older home on a top-tier 1-Acre lot in West Atherton, closing above $12M; three years later the same location was worth $18M+, a paper gain of roughly $6M (see our /en/cases library: the West Atherton three-year-appreciation case). Drop the $500K married exclusion into that pool and it covers under 10% of the gain—leaving about $5.5M that, if actually realized, would run the full gauntlet of long-term capital gains + NIIT + California's ordinary rate. Three years on, this family still holds and has not listed; at this magnitude, whether to realize the gain now and absorb that tax bill becomes part of the "sell or not" decision itself—selling was never only a question of price. Here, the $500K exclusion is close to a rounding error.

Now look at which end the lever sits on. A counterpoint from the other direction is a sale we ran this year in Midtown Palo Alto: an otherwise "unremarkable" single-family home, listed at $3.88M, closed at $4.38M—about $500K over, roughly +12.8%. The first instinct for many is "sell for $500K more, pay more tax, right?"—but keep two things apart. A higher sale price lifts the proceeds; the other half of what determines the taxable gain is whether you can substantiate cost basis and selling costs. In that deal the owner did three weeks of pre-list refresh and painting before going to market—and a reminder: painting and repairs alone generally do not add to basis; what does are additions, rebuilds, and system-level capital improvements. But commission and transfer tax and the rest of the selling costs are real deductions off the proceeds, shrinking the taxable gain directly. In other words, strong execution lifts the sale price, and strong tax preparation pushes the taxable gain down—do both, and the take-home nets out largest.

Common Mistakes

Mistake 1: "The $500K exclusion comes off the sale price"

No. Section 121's $250K/$500K reduces capital gain (sale price minus cost basis), not the total closing price. On a home that closes at $4.5M, if your cost basis (purchase price + capital improvements) is $2M and selling costs are $250K, the true gain is about $2.25M—and the exclusion comes off that $2.25M, not the $4.5M. Treating it as "sale price minus $500K" badly understates your taxable gain and sets you up for a shock when the tax bill lands (source: IRS Section 121).

Mistake 2: "I'm way past the exclusion anyway, so basis and commission don't matter"

The opposite is true—the more you exceed it, the more basis is worth. Taxable gain = (sale price − selling costs) − (purchase price + capital improvements) − exclusion. Every additional $100K of documented capital improvement you add to basis, and every commission / transfer tax / escrow fee you deduct off the proceeds, is $100K that never lands in that ~37% stack—about $37K of real money saved at the top. The move that matters is to archive the contracts, invoices, and permits from every year's remodel now, rather than rummaging for incomplete records at closing (source: IRS cost-basis rules).

Mistake 3: "An inherited home also owes a big capital-gains tax when sold"

Usually not. Inherited property gets its cost basis stepped up to the fair market value on the decedent's date of death (basis step-up). Which means if you sell shortly after inheriting, at close to market value, the taxable gain can be small or even zero—because the starting point for appreciation is reset to the moment you inherited, not the price your parents paid decades ago. This is a completely different mechanism from the "primary-home exclusion"; do not conflate the two. The specific figure depends on the estate valuation and any movement during your holding period (source: IRS inherited-property basis rules).

Mistake 4: "A home I once rented out is fully tax-free as long as I move back in for two years"

It is not that clean. The post-2009 "nonqualified use" rules reduce the gain you can exclude in proportion to the rental period as a share of the holding period—moving back in for two years only gets you over the eligibility line; it does not make the whole stretch of gain excludable. Watch a second point: if you claimed depreciation while the home was rented, that depreciation recapture sits outside the Section 121 exclusion and is taxed separately at up to 25%. Anyone who once rented, or converted an investment property to a primary home, should have a CPA break these two pieces out first (source: IRS Section 121 nonqualified use / depreciation recapture rules).

Next Steps

- Compute the "true gain" first, not the "paper appreciation": run (sale price − selling costs) − (purchase price + capital improvements) − exclusion, so you know what actually lands in the tax stack.

- Archive every year's remodel records now: contracts, invoices, permits—each documented capital improvement adds to basis and cuts the taxable gain directly at sale.

- Check your exclusion eligibility: confirm 2 years of primary-home use and 2 years of ownership within the five years before the sale, and that you have not used the exclusion in the past two years (once every two years).

- If there's rental / investment history, break out the special rules first: have a CPA compute the nonqualified-use proportion and depreciation recapture separately—neither is inside the exclusion.

- Read the timing of the sale together with your other income that year: a large gain pushes you into the federal 20% and California 13.3% top bands, so work with a CPA on staging the realization across years or offsetting it against other income—sometimes that saves a whole bracket.

Further reading: If you're selling an investment property, not a primary home—how a 1031 exchange defers the tax, A foreign seller's Bay Area sale and how the 15% FIRPTA withholding comes home.