Direct Answer

Because California's Prop 13 resets your home's assessed value to the price you paid the moment it changes hands—it does not continue the seller's decades-old low basis. Your purchase-year annual tax bill often still rides on that old, low number, and the county trues up the difference only later: that "supplemental assessment" notice, arriving months behind, catches up the tax your purchase price actually owes in a single stroke. A $10M purchase carries roughly $110K–$125K a year (at an effective rate around 1.1%–1.25%); the size of the catch-up bill turns on how far your new basis sits above the seller's old one.

This article is for decision-making education and does not constitute legal or tax advice; confirm the specifics with your attorney or CPA.

Who This Article Is For

- Buyers purchasing or touring at $5M+ on the Peninsula or in the South Bay who want the annual property tax and the transition-year catch-up bill built into the budget before they close.

- Cross-border high-net-worth buyers, used to a one-time transfer tax in their home market, meeting for the first time a structure where you pay tax on your purchase price every year and receive an extra bill after closing.

- Owners planning to buy land and rebuild, or to add substantially to an existing estate, who need to understand how the new construction is assessed on its own.

- Families holding a Bay Area primary home for the long run, who want to see how Prop 13's 2%-a-year cap grows more favorable the longer they hold.

Three Core Judgment Dimensions

At $5M+, property tax is not a "whatever the seller pays now is what I'll pay later" number. To size it correctly, read three dimensions.

One: the base year is anchored to your purchase price, not the seller's old ledger

California's Prop 13 (passed in 1978, Article XIII A of the state constitution) works on a single mechanism: at the moment a property undergoes a change of ownership, its base-year value is reset to the market value of that moment—for nearly every sale, that is your purchase price. The seller may have held for twenty or thirty years at a basis far below market, but that low basis does not travel with the house. Once title changes, the assessor takes your purchase price as the new starting line.

That is why two identical homes side by side can owe several times each other's annual tax—the only difference is who bought which year, and at what price. So pulling up what the seller currently pays tells you almost nothing when you tour; what actually sets your cost is your own purchase price times the effective rate.

Two: where the catch-up bill comes from—the supplemental assessment's lag, and why there can be two

This is where new buyers most often get caught flat-footed. California's fiscal year runs July 1 to June 30, and the annual roll is usually locked to the seller's old basis well before your closing. So your purchase-year annual bill often still shows the seller's low figure—but that is not what you actually owe.

After the fact, under the supplemental assessment rules in force since 1983 (SB 813), the assessor computes the difference between your new base and the seller's old one on its own, prorates it over the time left in the fiscal year, and sends you one—or two—supplemental assessment bills. Whether you get one or two depends on where in the fiscal year the sale falls; they typically land months after closing, because the assessor's office runs behind. Put plainly, this bill is not the county overcharging you—it trues up the portion escrow underbilled on the old basis.

Three: new construction triggers a second reassessment—the land keeps its old base, the new structure is entered on its own

Change of ownership is not the only trigger; new construction sets off a reassessment too. But its logic differs from a whole-property transfer: the land keeps its base-year value unchanged, and only the newly built or added structure is assessed separately at its market value on completion, given its own base-year value, and added to your taxable total as a supplemental assessment.

For anyone buying land to rebuild, or heavily renovating and expanding an older house, this belongs in the budget up front: you are not reassessing the whole asset at a new market value—you are stacking "the land at its prior base plus the new structure at a fresh base," the two summed separately. It is also why, in land-value-led markets like Atherton, the property-tax math on a teardown-and-rebuild has to be run as two figures projected apart.

Key Parameters and Typical Scenarios, Side by Side

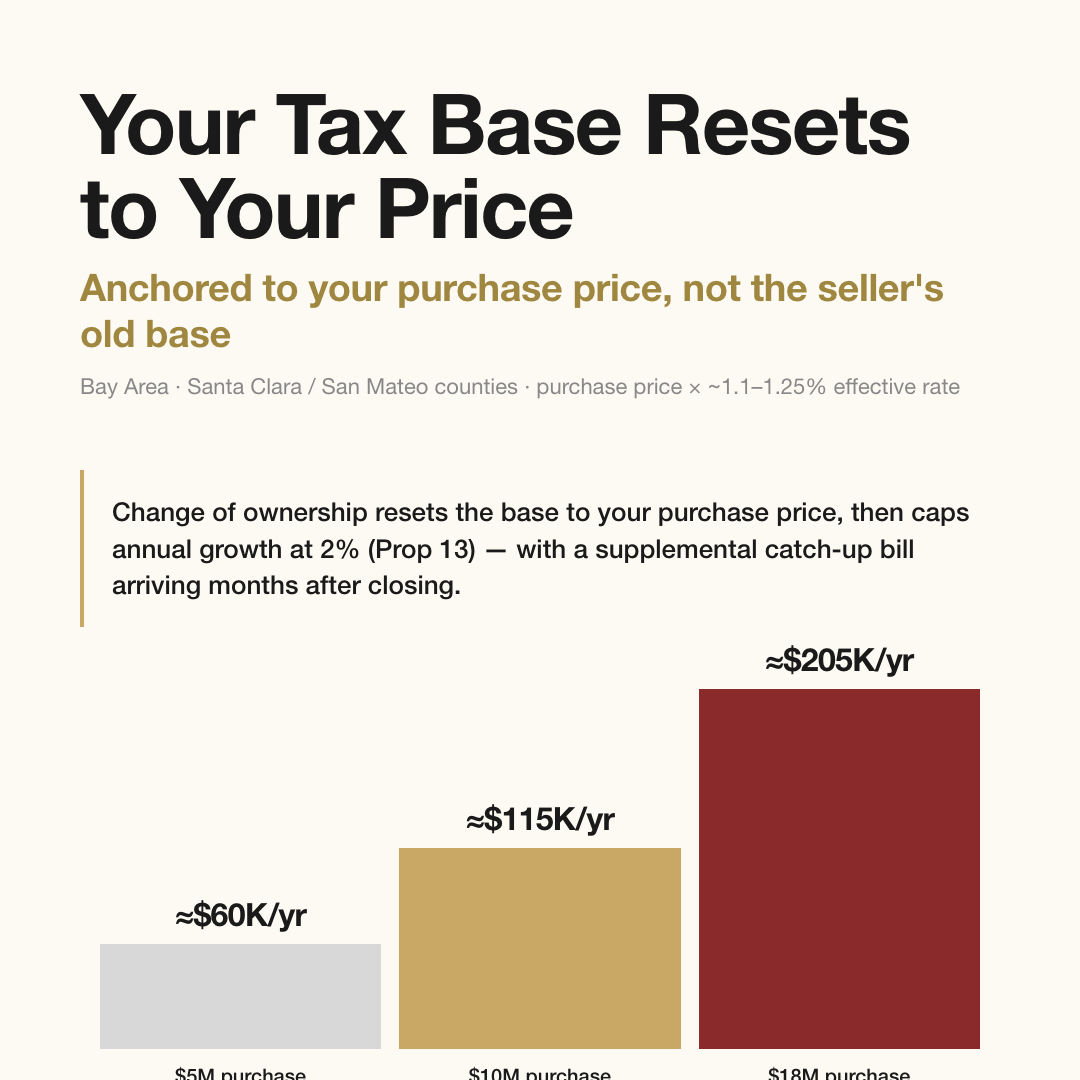

The core numbers first: Bay Area effective rates run about 1.1%–1.25% (the 1% base rate plus local and school-bond add-ons, varying by tax rate area), so a $10M purchase carries roughly $115K a year in property tax and $18M roughly $200K; your base is locked to your purchase price and climbs at most 2% a year thereafter. What blindsides new buyers is not the annual bill—it is the supplemental assessment that arrives months after closing, trueing up in one stroke the difference escrow underbilled on the seller's old basis.

| Item | Rule / Figure |

|---|---|

| Prop 13 base rate | 1% (Article XIII A, 1978) |

| Bay Area effective rate | ~1.1%–1.25% (1% + local / school-bond add-ons; varies by tax rate area) |

| How the base is set | Market value / purchase price at change of ownership or completed new construction (base-year value) |

| Annual increase cap | ≤ 2%/year (or CPI, whichever is lower) |

| Annual tax on a $10M purchase | ~$110K–$125K |

| Annual tax on an $18M purchase | ~$198K–$225K |

| Supplemental assessment triggers | Change of ownership + new construction / additions |

| Number of supplemental bills | 1 or 2, depending on where in the fiscal year the sale falls |

| When the supplemental bill arrives | Months after closing (assessor processing lag) |

| Fiscal year | July 1 – June 30 |

The thing to hold onto: the property tax collected through escrow is almost always estimated on the seller's old (low) basis, so it is not what you will actually owe going forward—your true annual base is your purchase price times the effective rate, with the gap closed by that late-arriving supplemental bill. Run the other way, the longer you hold, the more Prop 13's 2% cap works for you: when market value doubles over the years, your base still creeps up at most 2% a year, so a long-term owner's real tax burden relative to market value falls year over year.

Data sources: California State Board of Equalization (BOE) Prop 13 / SB 813 supplemental assessment rules / Santa Clara County Assessor / San Mateo County Assessor-Tax Collector / Article XIII A of the California Constitution.

Last updated: 2026-07

Scope: Property-tax base and supplemental assessment on $5M+ primary and investment residences in the Bay Area (Santa Clara / San Mateo counties).

The MK Group Field Observation

Across $5M+ transactions on the Peninsula and in the South Bay, MK Group's two founders, Marie Wang (DRE# 02110980) and Kevin Mo (DRE# 02127623), keep seeing the same blind spot: buyers treat "what the seller pays now" as their own future cost, then get caught off guard by the post-closing reassessment and the catch-up bill.

In an Atherton off-market deal that closed in May 2026, MK Group acted as buyer's agent for a cross-border buyer purchasing an architect-built estate at the $18M tier. The seller had held the home for years at a basis far below market; once title changed, the base reset to roughly $18M, and the annual property tax stepped up to the order of $200K (at an effective rate around 1.1%–1.25%). For a cross-border buyer used to a one-time transfer tax in their home market, the structure—pay on your purchase price every year, plus a transition-year catch-up bill after closing—has to be laid out in advance. MK Group built that annual carrying cost and the supplemental assessment's timing into the buyer's cash-flow plan during execution, rather than explaining it once the bill arrived.

The base-anchored-to-purchase-price point shows up most plainly in families with a clear brief. One family budgeting $10M+ settled in Atherton—their requirements precise: a large living room for entertaining, a private garden, close to Stanford and Sand Hill Road—and their base locked to that $10M+ purchase price, an annual tax of roughly $110K–$125K, climbing at most 2% a year thereafter and gradually decoupling from what the market will be a decade on. This is exactly Prop 13's dividend for the long-term owner: the earlier your purchase price is locked in, the better the deal reads over time.

New construction and additions trigger a second reassessment. MK Group assisted a cross-border high-net-worth buyer purchasing a 2-acre new-build in Atherton at about $13.5M, mapping out an SB9 lot-split and rebuild path for the future. The key property-tax logic here: the land's base-year value is fixed at purchase, while any structure built afterward is entered separately at its completion-date market value with its own base-year value—"the land keeps its old base, the new structure gets a fresh one," the two summed into your taxable total. For anyone planning to buy land and rebuild or add substantially, this "new-construction supplemental" belongs in the budget from the start.

(All cases above are anonymized; identities, exact addresses, and family details are blurred. The price tiers, funding structures, and features—cross-border buyer / off-market / 2-acre new build / SB9 lot split—come from real transactions in MK Group's own record. The annual property-tax figures are estimates of purchase price times the published effective rate.)

Common Mistakes

Mistake 1: "The tax on this home just runs at whatever the seller has been paying"

No. Under California's Prop 13, the base resets to your purchase price the moment ownership changes, and the seller's decades of accumulated low basis do not travel with the house. The "seller currently pays $X in tax" you pull up while touring only reflects which year they bought and at what price—of almost no use to you. What sets your cost is your own purchase price times the effective rate: a $10M purchase carries roughly $110K–$125K a year, an $18M purchase roughly $200K (source: County Assessor / CA Prop 13).

Mistake 2: "The tax collected through escrow is everything I'll owe each year"

Not so. The property tax collected at the escrow / impound stage is almost always estimated on the seller's old (low) basis, because your purchase-year annual roll is usually already locked. Months after closing, under the supplemental assessment rules (SB 813), the assessor computes the difference between the old and new bases on its own, prorates it over the time left in the fiscal year, and sends one or two supplemental assessment bills. This is not the county overcharging—it trues up the portion underbilled on the old basis. At $10M+, the supplemental bill is routinely six figures, so reserve the cash for it in advance (source: California BOE / SB 813).

Mistake 3: "As long as I hold, the tax rises with the market every year"

Wrong—the opposite, in fact. Prop 13 caps the annual increase in your base at 2% (or CPI, whichever is lower), decoupled from market swings. When Bay Area prices double over a stretch of years, your base still creeps up at most 2% a year—the longer you hold, the lower your real tax burden relative to market value. This is Prop 13's most tangible dividend for the long-term owner, and where the compounding value of "buy early, lock the base-year value" lives in a high-appreciation market (source: CA Prop 13 assessment-cap rules).

Next Steps

- Pull the currently recorded assessed value on your target home (the county assessor's site shows it) and measure the gap to your expected purchase price—the wider the gap, the larger the supplemental bill, so never budget off the seller's old figure.

- Fold the property tax into the full carrying cost: the annual tax is only one line—insurance, maintenance, Mello-Roos / HOA all sit alongside it, and only together do they tell you the true monthly cost. See the real all-in cost of owning a Bay Area home.

- Before closing, get escrow / your lender to state plainly whether the tax collected in impound is estimated on the old basis or on your purchase price, and set aside extra cash for the supplemental bill (routinely six figures at $10M+).

- If you plan to buy land and rebuild or add substantially, confirm with the county assessor or a tax professional up front how the new construction's supplemental assessment and completion timing are handled—project "the land base plus the new-structure base" as two separate figures.

- If you are moving at 55+ or a parent-child transfer is involved, the base may be able to transfer rather than reset—that is a separate set of rules. See how much Prop 19 can actually save on a Bay Area 55+ move.